What is a credit score, and how can this score help you in your everyday finances? Learn more about how to evaluate and build your own score.

Creditworthiness is a common factor in determining approval for loans, credit cards, and other things you could need to apply for one day. Learning more about how good credit and bad credit work and studying the following helpful credit score charts and credit score tips can really help you use credit scores to your own advantage and build yourself an excellent credit score. Debt Consolidation could be a good way to boost your score.

Credit Scores Explained

How do credit scores work and how do they relate to everyday finances? If you've never thought about it before or are currently looking for loans for bad credit, then credit scores can seem complicated and hard to understand. But, it's actually very simple once you understand these credit score basics.

The purpose of credit scores is to help lenders make loan application decisions quickly and easily. This helps the loan application process go faster and smoother for both the borrower and the lender.

But what impacts your credit score? What determines someone's creditworthiness? Your credit score is mainly determined by the following information in your credit report:

Information in your credit report:

- Payment history

- Length of credit history

- Debts

- Current debts and loans

- Types of credit

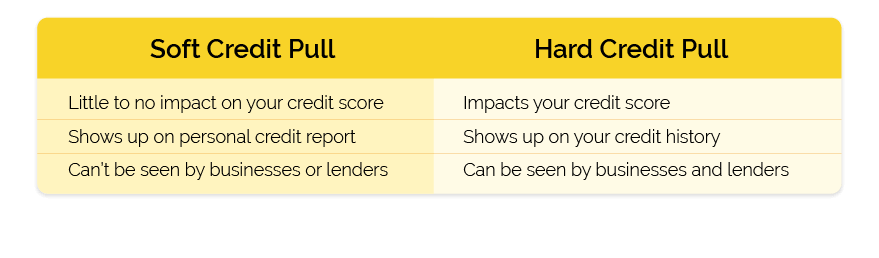

There are also important things to know regarding credit pulls. There are soft credit pulls, and hard credit pulls.

Soft Credit Pulls

A soft credit pull is a less intense credit report check. They tend to have less impact on your credit history, score, or report. They only appear on your personal credit report but won't be seen by businesses or lenders.

A soft pull might be initiated by someone else rather than yourself since this type of credit pull won’t hurt your overall score. Soft pulls also tend to have little to no impact on your credit score because they are a less intense report.

Hard Credit Pulls

A hard credit pull is a more intense credit report check. They tend to have more impact on your credit history, score, or report than a soft pull. Hard pulls usually show up on your credit history for businesses and lenders to see.

A hard pull is usually initiated by you when submitting some kind of application, usually for credit like a loan. Hard pulls also tend to have more impact on your credit score because they are a more intense report.

Subprime Loans vs Prime Loans

Subprime and prime are terms that refer to the range of rates for a loan.

Prime rates are some of the best loan rates, but they also have more requirements to qualify for prime loans, like higher credit scores. But these types of loans can also provide higher credit limits.

Subprime rates are higher interest rates but are generally attached to loans that are easier to qualify for and come with fewer requirements for acceptance.

These types of loans come with more credit risk for the lender, though, so your subprime credit account might not have the high balance available with a prime credit account. But you also won’t necessarily need a higher credit score either.

What is a subprime loan?

Subprime loans and subprime lending is known by many names. It can also be called near-prime, subpar, non-prime, or second-chance lending. Subprime loans are designed for customers who have difficulty qualifying for premium loans with higher application requirements, like high credit scores.

If you are taking out a subprime loan, then remember that your subprime credit report score is not the same thing as your FICO® score. Contact your lender directly for more details.

Credit Score Charts

Equifax, TransUnion, and Experian are 3 examples of major credit reporting agencies a lender might use. Many credit reporting bureaus also have different credit score ranges and scoring models set up for different industries. But with any credit bureau, your score is a number out of a larger number range.

Equifax Credit Score Range:

Equifax uses a number system from 300 to 850 to score creditworthiness. A credit score of 300 is the poorest score, and 850 is the best score.

Equifax Scoring Model:

- Poor: 300–579

- Fair: 580–669

- Good: 670–739

- Very Good: 740–799

- Excellent: 800–850

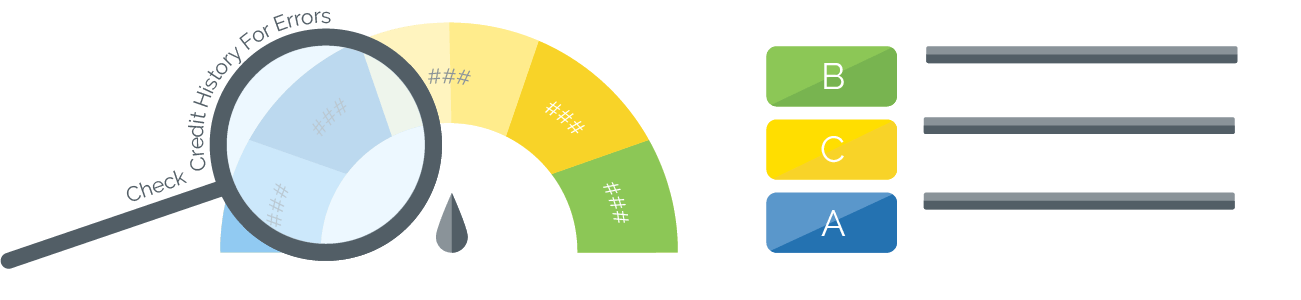

TransUnion Credit Score Range:

TransUnion uses a grading system from A to F to grade creditworthiness. This grading system is based on a number system from 300 to 850.

TransUnion Scoring Model:

- Grade A: 781–850

- Grade B: 720–780

- Grade C: 658–719

- Grade D: 601–657

- Grade F: 300–600

Experian Credit Score Range:

Experian uses a similar number range to Equifax.

Experian Scoring Model:

- Very Poor: 300-579

- Fair: 580-669

- Good: 670-739

- Very Good: 740-799

- Exceptional: 800-850

Remember that different lenders use different credit reporting agencies. Ask your preferred lender about where you should get your credit report for the best results.

What is a Bad Credit?

Knowing where you stand now can help you determine what is lowering your score so you can work on raising your credit. There are many factors that can cause someone’s credit score to be lower. The following list has a few examples of what could cause a bad credit score.

Common Bad Credit Causes

- Makes late payments

- Have more debt than you can afford

- Default on a loan

- Have filed for bankruptcy

- High credit utilization rate

What is a Good Credit Score?

To get a good credit score you need to avoid the pitfalls that cause bad credit in the first place. The common causes of bad credit lead to more loan denials and adverse actions because they tell lenders that you might be at a higher risk of defaulting or making late payments on a loan if they decide to lend to you.

You can increase your credit score and your chances of getting the loan you want by fixing these same issues.

How to Improve Good Credit:

- Make payments on time

- Keep your debt-to-income ratio at a safe level

- Avoid defaulting on loans

- Avoid bankruptcy

- Have a low credit utilization rate

Taking full control of your finances, budgeting effectively, and preparing for financial emergencies ahead of time can all help you avoid these negative credit marks and keep your credit score high.

How to Improve Credit Score

Even before shopping for a loan, it's a good idea to check your credit history for yourself. That way, you can have an idea of the kinds of loans you can qualify for before you start applying.

Checking your credit score yourself, before you apply, can also help you catch any mistakes on your credit history so those can be corrected before the lender pulls their own credit check.

Here are some of the main steps you want to take before taking out a loan:

Step 1: Get a copy of your credit history and do a self-audit

Go through your credit history and make sure there aren't any errors that need correcting before you start applying for loans.

You should check your credit report carefully for accounts you did not open, inquiries from creditors you didn't initiate, and any other errors or discrepancies you might find.

If you find something on your credit report that you do not understand, call the credit agency.

Step 2: Make sure nothing is missing on your credit report

If you have an instance that should be helping boost your credit and you can't find it on your credit report, contact the credit reporting agency to get it sorted out.

Certain things help give people good credit:

- Making payments on time

- Pay off a loan balance

When you have good credit actions in your personal finances, you want to make sure those actions are being counted in your favor on your credit report.

They are all instances that will boost your score and show potential lenders that you are a low-risk customer who knows how to pay their bills on time.

Credit can be your friend or your foe depending on how well you use it:

Make payments on time and make sure on-time payments are being counted on your credit history.

If you need help establishing a good credit history, you may consider paying for groceries each week with a credit card. At the end of each week, you can then pay off the credit card balance from paying for groceries to reset your revolving credit.

This content is for informational purposes only and does not constitute financial or legal advice. Loan products, terms, amounts, rates, fees, and funding times may vary by state and applicant qualifications. All loans are subject to approval and verification under applicable law. Check City is a licensed lender in each state where it operates. Loans are intended for short-term financial needs only. Please borrow responsibly.