The difference between prime lending and subprime lending is that prime lenders hold less risk than subprime lenders and offer different loan rates.

When shopping on the mortgage market, or for anything from credit cards to loans to home equity lines of credit, your credit score level is an important factor. This credit level helps financial providers know your borrower risk profile. This then determines whether you can apply for prime lending or subprime lending.

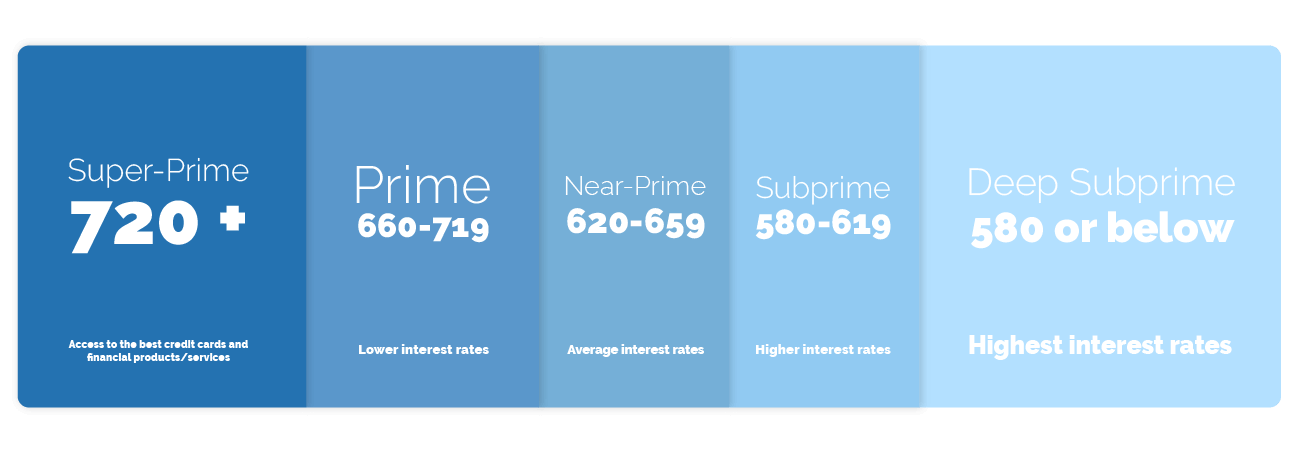

The 5 Credit Score Levels

There are many ways to categorize loans and borrowers and one of them is the 5 credit score levels. These 5 levels each come with a different credit score range and borrower risk.

Borrowers with higher credit scores are considered prime borrowers and can apply for prime lending with better rates and terms. Meanwhile, borrowers with lower credit scores are considered subprime borrowers and can apply for subprime lending with higher rates.

- Super-prime: 720+ FICO credit score

- Prime: 660-719 FICO credit score

- Near-prime: 620-659 FICO credit score

- Subprime: 580-619 FICO credit score

- Deep subprime: 580 or below FICO credit score

There are 5 different credit score levels or borrower risk levels, but the main levels you'll see most often are prime lending and subprime lending.

This terminology can be used to describe different kinds of lenders and the kinds of loans they offer. For instance, prime lending offers prime loans and subprime lending offers subprime loans.

Likewise, these different kinds of loans come with different levels of interest rates. So super-prime borrowers can qualify for the best, super-prime interest rates. These rates will be lower than the prime, near-prime, subprime, or deep subprime interest rates.

This is because the higher your credit score, the less risk you pose to lenders. When you have a low borrower risk, you can get rewarded with better rates.

What is Super-Prime Lending?

Super-prime lending involves the funding of super-prime loans to borrowers who have the highest credit scores. These types of borrowers have pristine credit histories and access to some of the best credit cards and other financial products and services.

According to the Consumer Financial Protection Bureau (CFPB), in November 2018 there were approximately 3.9 billion super-prime student loans opened.

What is Prime Lending?

Prime lending involves the funding of prime loans to borrowers who have average credit scores. These types of loans are generally helpful for borrowers with higher income qualifications who can get approved for prime loans. These loans will have lower interest rates.

According to the Consumer Financial Protection Bureau (CFPB), in November 2018 there were approximately 2.4 billion prime student loans opened.

What is Near-Prime Lending?

Near-prime lending involves the funding of near-prime lines of credit to borrowers who almost have prime level credit scores, but not quite. These types of loans are generally helpful for borrowers with average credit scores. These loans will have average interest rates.

According to the Consumer Financial Protection Bureau (CFPB), in November 2018 there were approximately 1.5 billion near-prime student loans opened.

What is Subprime Lending

Subprime lending involves the funding of subprime loans, such as payday loans, to borrowers who have below average credit scores. These types of loans are generally helpful for borrowers with lower income qualifications who might have a hard time getting approved for other loan types above subprime. These loans will have higher interest rates.

According to the Consumer Financial Protection Bureau (CFPB), in November 2018 there were approximately 1.0 billion subprime student loans opened.

What is Deep Subprime Lending?

Deep subprime lending involves the funding of deep subprime loans to borrowers who have the lowest credit scores. These types of loans are generally helpful for borrowers with low income who can't get approved for many other loan types. These loans will have the highest interest rates.

According to the Consumer Financial Protection Bureau (CFPB), in November 2018 there were approximately 1.9 billion deep subprime student loans opened.

Subprime vs Prime Rates

The closer you are to super-prime, the best rates you can get. But those who can't meet the stricter qualifications required for prime rates today can look into subprime options that are easier to qualify for.

One way to see the difference between subprime vs prime rates is to compare subprime mortgages with current prime rates for mortgages. Current subprime mortgage rates can range between 8% and 10% while current prime mortgage rates can range between 3% and 5%.

How to Get the Best Rates

If you want to get the best rates then you want to create a good credit history for yourself. Your credit history affects your credit score, which affects your credit level, which affects the credit and interest rates available to you. So, you want to create a pristine credit history for your finances, so that your credit score gets higher, so that your credit level improves, so you can get great credit and interest rates.

If you are a subprime borrower looking to become a prime borrower, then start with looking at your current financial situation and your budget.

Making on time payments is the primary key to building good credit. Make adjustments where necessary so you can start paying down debts, saving up, and paying all your monthly bills on time.

Avoiding having too many lines of credit out at one time is another great way to build up your credit score. You don't have to avoid loans and credit cards all together though, just make sure that during the life of the loan you are always making on time payments.

Access prime lending and move up from subprime lending when you make payments on time and avoid defaulting on any loans.

In Conclusion,

Building your credit level can open many financial doors to you. With great credit you can access great lines of credit and great rates. The higher your credit level, the easier your financial life will be in the housing market when you go shopping for mortgage lenders. Not only can it help you get a great mortgage loan, but it can help you in a financial crisis too when you need emergency funding with great rates. Great credit levels can even get you better credit cards with more perks and points.

This content is for informational purposes only and does not constitute financial or legal advice. Loan products, terms, amounts, rates, fees, and funding times may vary by state and applicant qualifications. All loans are subject to approval and verification under applicable law. Check City is a licensed lender in each state where it operates. Loans are intended for short-term financial needs only. Please borrow responsibly.