Learn more about the revolving credit definition and how you can take advantage of a line of credit to boost your credit score.

Credit can be a great burden or a great asset depending on how you use it. By using credit responsibly, you can have access to the funds you need while also building up your credit score as you repay those funds.

Make revolving credit yourfriend and not your enemy by how you use it. Use credit responsibly and takeadvantage of unique perks and benefits. You can also take advantage of a way tobuild your credit score up as you make on time payments.

Revolving Credit Definition

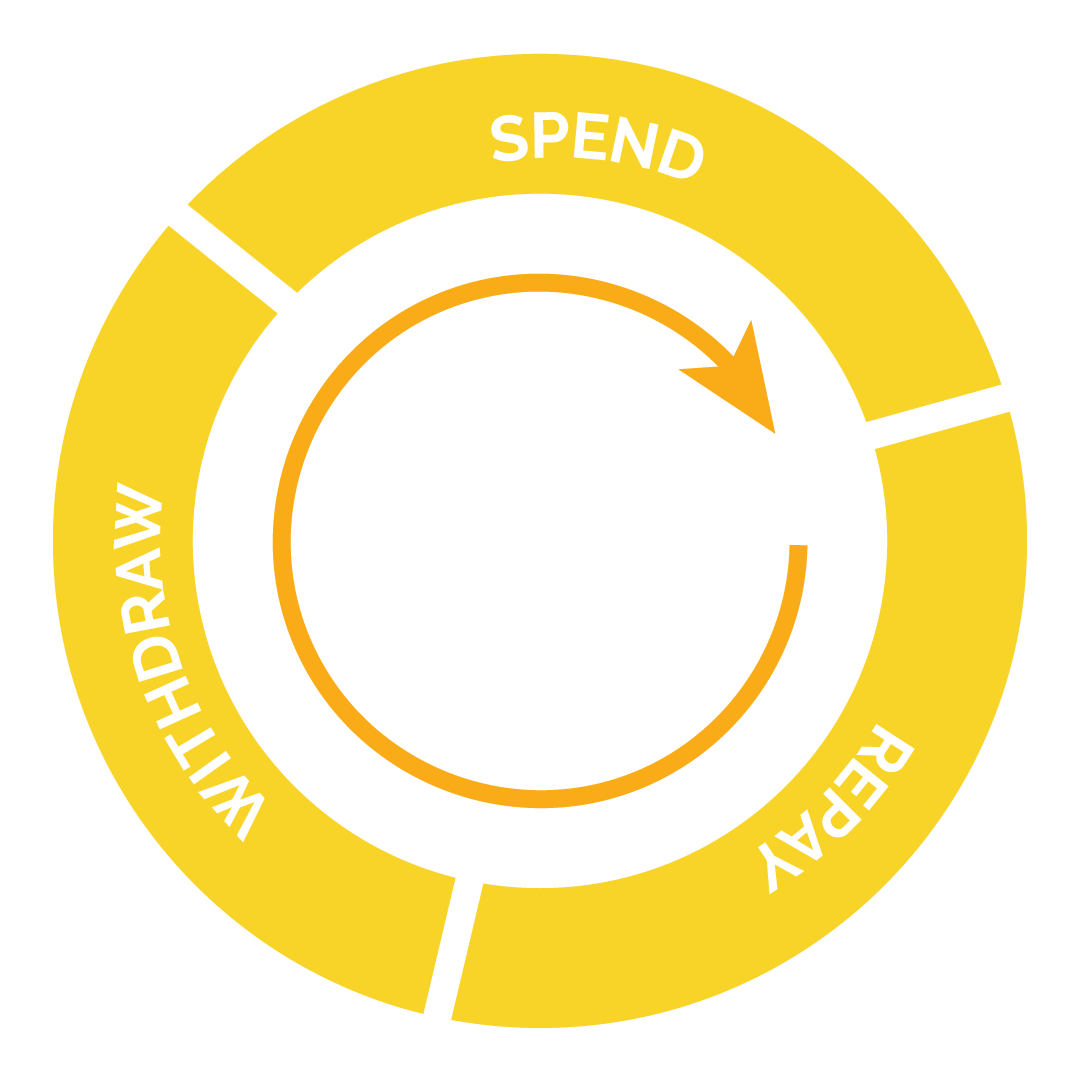

Revolving credit is when someone has access to a set dollar limit of funds that they can borrow from at any time. The most common type of revolving credit is a credit card. Someone with a credit card account might have revolving credit available on that card for $1,000. This means that this account holder can spend this $1,000 and pay if off repeatedly.

What is a Revolving Line of Credit?

Revolving credit and lines of credit are words that are closely related to each other. For instance, the $1,000 of revolving credit that someone has available on their credit card could also be referred to as a line of credit. Because it can be used over and over again, it is a revolving line of credit.

This line of credit has the protentional to increase as you use it and pay what you used off on time each month. Revolving lines of credit can also come with lots of other financial perks and benefits like payback rewards for whenever you repay part of the credit borrowed.

What is Revolving Credit?

Revolving credit is another word that can be used to describe credit funds that are always available to use and repay as the credit account holder sees fit. The term revolving credit specifically refers to the fact that this type of credit funding does not have a fixed number of payments to pay off the borrowed funds.

Instead, how much a credit account holder needs to pay back will depend on how much of the credit has currently been used. The line of credit is always there though, so there isn't a definitive amount of repayments that need to be made for the borrowed funds to be "paid off" the way you would with a loan.

How Does Revolving Credit Work?

The revolving credit process begins with a revolving credit account. This could be a lender or a bank or another kind of financial institution. This line of credit provider will have accounts that customers can apply for. This might be a personal line of credit account or a more common credit card account. The application for these lines of credit might include a credit report check too.

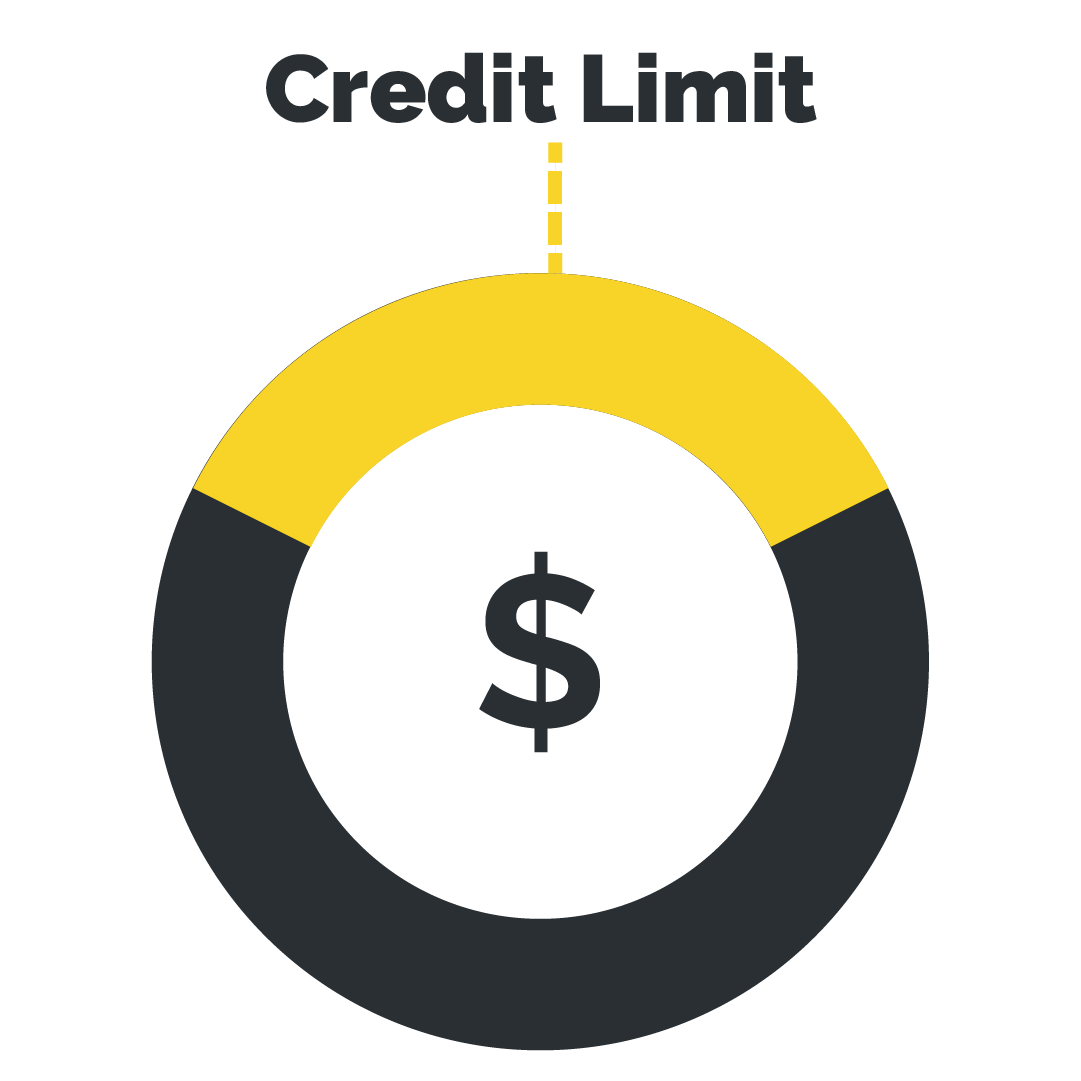

Once you are approved for the line of credit account, you'll be given a maximum amount on the account that you can spend. This credit amount is your "line of credit."

Credit accounts come with a monthly billing cycle and interest rates. The longer you wait to repay the money you borrowed from the account, the more that interest rate will accumulate and increase how much you need to pay back. Often, if you pay back what you borrow before the end of each billing cycle, you can avoid this interest rate.

Some accounts will come with additional fees as well like an origination fee for starting the account or an annual fee for maintaining the account. To use a form of revolving credit responsibly, you want to make sure the ratio between your total credit used and total credit available, also known as your credit utilization rate, stays lower than 30%.

Revolving Credit Examples

Revolving credit lines can be a great way to have access to extra funds whenever you might need them. There are a few revolving credit examples that you could choose from to get the extra funding you need.

Credit Cards

Credit cards are probably the most common form of revolving credit. Credit cards will come with an interest rate, a credit limit, and a structure for minimum repayments as you use the credit available on your card. Credit cards can be a great way to earn cash back rewards and other cool rewards as you use and pay off the funding you borrow.

Personal Line of Credit (PLOC)

A personal line of credit is different from a credit card in that you don't get to keep that line of credit forever. You have a set limit that you can use and a set limit to how long you can use it. This is called your draw period.

This type of credit set up can be nice for when you might need extra money, but you don’t want to take out a lump sum loan all at once. So you can take out the funds you actually need, as you need them.

Home Equity Line of Credit (HELOC)

A home equity line of credit is just like a personal line of credit, but the loan collateral for the loan money is the equity of the borrower's house.

Just like with a personal line of credit, a lender makes a certain amount of credit available to the borrower. The borrower can then take out the money they need from that maximum amount as they need it. These funds are also only available during a set draw period.

Open-Ended vs Close-Ended Line of Credit

Some forms of credit can be open ended while other are close ended. These finance terms refer to how the credit is taken out and how it is repaid, or rather, the kind of access the borrower has to the line of credit funds.

An open-ended line of credit gives the borrower access to any amount of the available money at all times. This type of credit might still have a set draw period, but there are no required lump sums involved. Credit cards, personal lines of credit, and home equity lines of credit are all examples of open-ended lines of credit.

A close-ended line of credit gives the borrower limited access to the available money for a limited amount of time. This type of credit gives the borrower a lump sum of money that they then have to repay in a set schedule of monthly payments to pay off the balance in full. Personal loans and installment loans are some examples of close-ended lines of credit.

This content is for informational purposes only and does not constitute financial or legal advice. Loan products, terms, amounts, rates, fees, and funding times may vary by state and applicant qualifications. All loans are subject to approval and verification under applicable law. Check City is a licensed lender in each state where it operates. Loans are intended for short-term financial needs only. Please borrow responsibly.