Freezing your credit is one of the most effective ways to protect yourself from identity theft. It’s free, doesn’t affect your credit score, and can be done in minutes with Equifax, Experian, and TransUnion.

In 2024, there were over 1 million reports of identity theft in the United States. Having your identity stolen can have devastating financial effects, from drained accounts to a ruined credit score that hurts your ability to access competitive loans. It’s frightening and costly.

One of the best steps you can take to protect yourself against the financial hardship of identity theft and fraud is freezing your credit. Discover how to freeze your credit with all three credit bureaus in this simple step-by-step guide.

What is a Credit Freeze?

When you put a credit freeze in place, it means that no one can open new lines of credit in your name. Any scammers falsely applying for loans will automatically be rejected if you freeze your credit report. Since identity theft and threats like IRS scams are increasingly common, it’s worth taking steps to protect yourself.

The good news is that credit freezes are free and available from all three major credit bureaus. You just need to know how to freeze your credit with each one, since the steps are slightly different.

Implementing a credit freeze does not hurt your credit score. Just keep in mind that a credit freeze also prevents you from opening new lines of credit, and it doesn’t stop financial scammers from using your current cards or hacking your existing accounts.

Why You Might Want to Freeze Your Credit

There are lots of scenarios that might prompt you to freeze your credit, such as:

- Noticing unusual activity on your accounts

- Losing your wallet

- Receiving a data breach notification

- Wanting more peace of mind about identity theft

As you’re building your credit, you don’t want a scammer opening new credit lines in your name. Placing a credit freeze is like putting a lock on your front door; it’s extra protection to keep criminals out. Identity theft is stressful, and this is a powerful protective step.

How to Freeze Your Credit, Step by Step

To prevent anyone from viewing your credit report and potentially opening new credit accounts in your name, you need to freeze your credit at each of the three major credit bureaus. Learn how to freeze your credit at each one with these simple steps.

Freezing Credit With Equifax

Each credit bureau offers the option to freeze your credit online or by phone. If you’d prefer to complete the process over the phone, call Equifax at 1-800-349-9960 and follow the steps described by the Equifax agent. Otherwise, complete this online process:

- Go to https://www.equifax.com/personal/credit-report-services

- Select "Freeze your Equifax credit report."

- You’ll need to provide personal information, like your name, date of birth, Social Security number, and address.

- Create an account with your email address and a secure password. Make sure you write these details down so you can get back into your account easily later.

- Equifax will send you a six-digit code to your phone at the mobile number you provided. Enter that code on the sign-up page to verify your identity. You’ll see confirmation that your account setup is complete.

- Once you’re signed in, select “Place a freeze.” Confirm that you want to place a freeze on your Equifax credit report.

Your security freeze will then activate, and you'll have the option to download a PDF confirmation. If a lender contacts Experian to pull your credit report while you have this freeze in place, they will simply be notified that your credit is frozen and access is denied.

Freezing Credit With Experian

Next, head to Experian to freeze your credit there. Once again, you can freeze your credit over the phone by calling Experian at 1-888-197-3742, or you can use these steps to complete the process online:

- Go to https://www.experian.com/help/credit-freeze/

- If you don’t have an account, select “Create a free account.” If you do have an account, sign in.

- Provide the last four digits of your Social Security and mobile phone number. This information is only used for verification purposes.

- Click on the link that Experian texts your phone to verify your device, then head back to your original device.

- Enter your personal information and double-check that everything is accurate.

- Choose a free membership, unless you’d like additional paid services from Experian, and create an account with your email address and password.

- You’ll need to select and answer a security question and create a four-digit PIN.

- Experian will show that your file is unfrozen. Select “Frozen” instead to freeze your Experian credit file.

- You’ll see confirmation that your credit was successfully frozen.

If you need to unfreeze your credit sometime in the near future, you can “schedule a thaw” for a specific date. Otherwise, there’s nothing left to do. Your Experian credit file will stay frozen until you unfreeze it.

Freezing Credit With TransUnion

Finally, complete the last credit freeze with TransUnion by calling 1-888-909-8872 or following these steps online:

- Go to https://www.transunion.com/credit-freeze

- Select “Add Freeze.”

- If you have an account, sign in. If not, create a free account by providing details like your name, address, phone number, and the last four digits of your Social Security number.

- Create a username and password for your account.

- Choose a secret question and answer it. Write down your answer in case you forget it.

- Choose to receive a one-time passcode through a text message or phone call. Enter the five-digit passcode you received via the method you chose.

- Once you’re signed in, select “View my freeze status” under “Credit Freeze.”

- Select “Add Freeze” and “Continue.”

- You’ll see a confirmation that your TransUnion credit report is now frozen and receive a confirmation email.

How to Lift or Remove a Credit Freeze

You can leave a credit freeze in place as long as you want to stay protected. However, there are some situations when you might want to remove a freeze — basically, any time you want to open new credit lines.

For example, if you’re applying for a car loan or mortgage, lenders will need to be able to pull your credit report, so you’ll have to unfreeze your credit. Similarly, if you’re applying for a new credit card, you need to remove the credit freeze at all three credit bureaus.

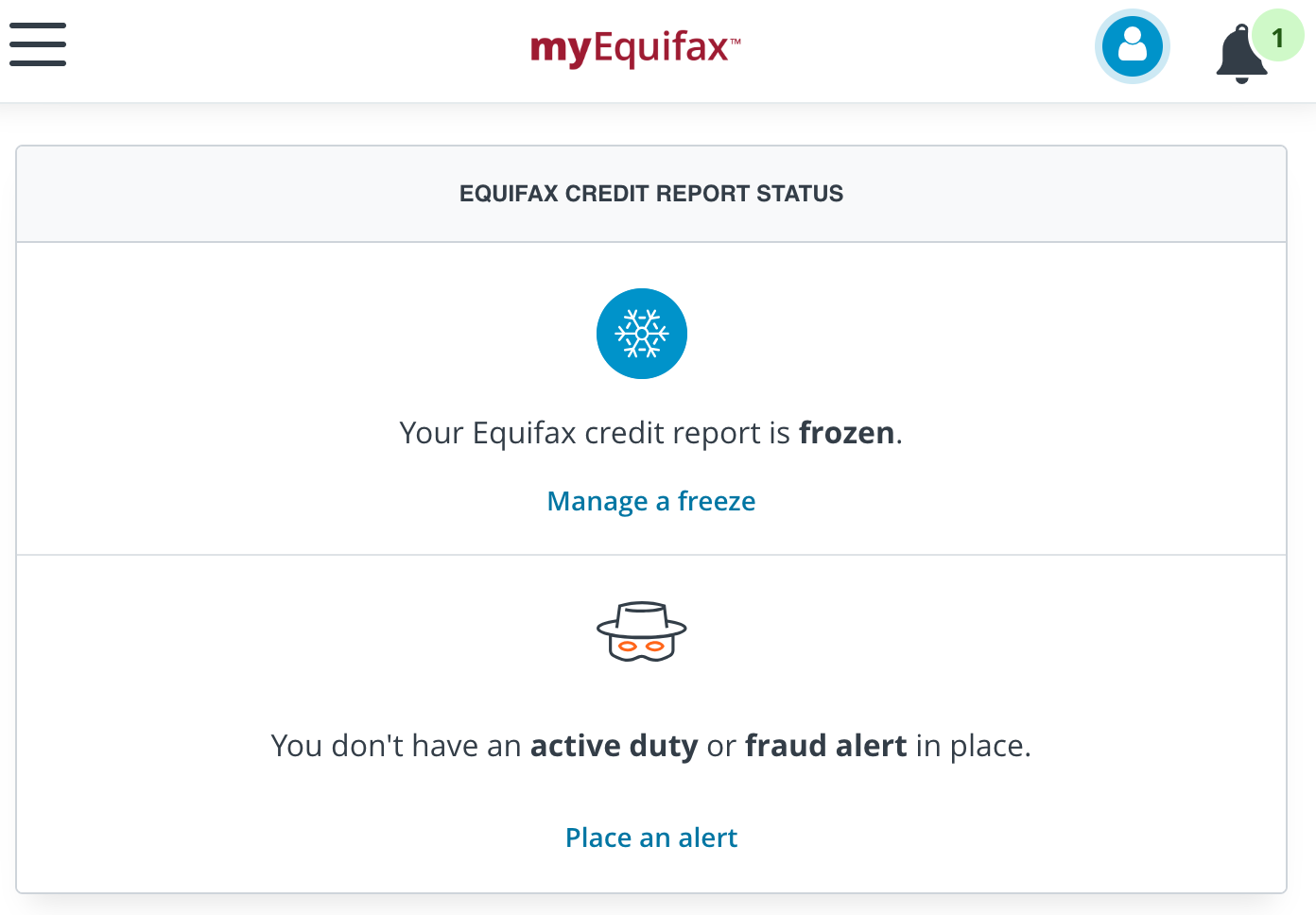

How to Unfreeze With Equifax

- Go to https://www.equifax.com/personal/credit-report-services

- Log in to your account.

- Under “Equifax Credit Report Status,” select “Manage a freeze.”

- Choose whether you want to temporarily lift the credit freeze or remove it permanently.

- Confirm that you want to remove the freeze.

You should see confirmation that you successfully removed the credit freeze from your Equifax credit file.

Alternatively, you can call Equifax at 1-800-349-9960 to remove your credit freeze.

How to Unfreeze With Experian

- Go to https://www.experian.com/help/credit-freeze/

- Log in to your account.

- Under “Freeze your Equifax credit report,” select “Manage a Freeze.”

- Select “Unfrozen.”

- You’ll see confirmation that your credit file was successfully unfrozen.

If you’d prefer to unfreeze your credit file with Experian over the phone, call 1-888-197-3742.

How to Unfreeze With TransUnion

- Go to https://www.transunion.com/credit-freeze

- Log in to your account.

- Under “Credit Freeze,” select “View my freeze status.”

- Choose either “Remove Freeze” or Temporarily Lift Freeze.”

- If you’re only lifting the freeze temporarily, indicate when you want the freeze to go back into place.

- Confirm that you want to remove your TransUnion credit freeze.

You can also call 1-888-909-8872 to unfreeze your TransUnion credit file.

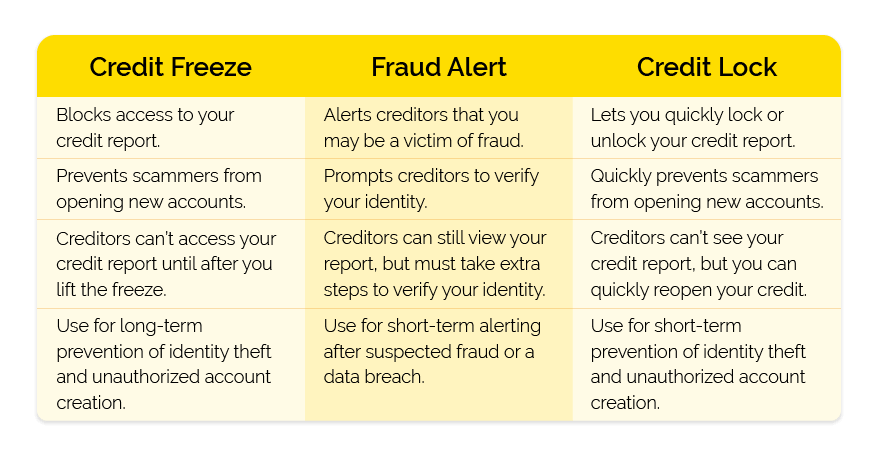

Credit Freeze vs Fraud Alert vs Credit Lock

A credit freeze isn’t the only way to protect yourself against fraud. While a credit freeze establishes a complete stop on new credit in your name, a fraud alert is a less extreme security option.

If you put a fraud alert in place, lenders must more thoroughly verify the identity of anyone applying for a new line of credit in your name. So, you can still open new credit, but there are additional obstacles for fraudsters than if you didn’t have the fraud alert in place.

Your other option is a credit lock, which is typically managed through a mobile app. It’s not as strong as a credit freeze and may be part of a paid credit monitoring subscription.

If you’re struggling to decide which of these options is the best way to protect your finances, reach out to Check City. Our experts can help you find the ideal solution for your needs.

How Credit Freeze Affects Your Financial Life

Putting a credit freeze in place has no impact on your credit score; it won’t go up or down as a direct result of the freeze.

You can still use your existing credit cards, pay bills, and get approved for new jobs or apartments with the freeze in place. However, you’ll have to lift the freeze to apply for new credit, like a mortgage or a new credit card.

When a Credit Freeze Makes Sense

A credit freeze makes sense for most people who don’t plan to apply for more credit soon. If you’ve recently been a victim of identity theft or had data exposed, freezing your credit is even more important.

For those who often open new credit accounts, freezing and unfreezing your credit may become tedious. In that case, you could implement a fraud alert instead to protect your credit. Another option is using credit monitoring services to catch scammers right away if someone’s trying to open unauthorized accounts in your name.

FAQs About Freezing Your Credit

Can I freeze my child’s credit?

Yes, you can freeze your child’s credit if they are under 16 years old.

How long does a credit freeze last?

A credit freeze lasts indefinitely until you choose to lift or remove it.

Do I have to freeze my credit at all three bureaus?

Yes, you should freeze your credit at Equifax, Experian, and TransUnion. If you only freeze your credit with one or two of the bureaus, your credit could still be at risk.

What’s the difference between a “credit freeze” and a “freeze warning”?

A credit freeze is a process you can take to completely block access to your credit report for new credit applications. A freeze warning, in contrast, is a type of fraud alert that tells lenders to take extra steps to verify your identity.

Does it cost money to freeze my credit?

No, freezing your credit is free at all three major credit bureaus.

How Check City Supports Your Financial Security

Check City is committed to increasing financial literacy and helping customers feel confident with the money decisions they make. While we don’t manage credit freezes directly, we do provide education, guidance, and tools to help you protect your finances, such as:

- Tips on identity theft prevention

- Credit report guides

- Articles on budgeting and ensuring your financial wellness

The Bottom Line

It only takes a few minutes to protect yourself against identity theft by freezing your credit at all three major credit bureaus. You can always unfreeze your credit later whenever you need to apply for new accounts.

Key Takeaways:

- Credit freezes block new accounts from being opened in your name, stopping scammers cold.

- They’re free, permanent until lifted, and don’t impact your credit score.

- You’ll need to unfreeze your credit before applying for loans, credit cards, or mortgages.

- Freezes don’t protect existing accounts; continue monitoring your cards and bank activity.

- Fraud alerts and credit locks are alternatives but generally less secure than a freeze.

- You can also freeze your child’s credit (under 16) for added protection.

This content is for informational purposes only and does not constitute financial or legal advice. Loan products, terms, amounts, rates, fees, and funding times may vary by state and applicant qualifications. All loans are subject to approval and verification under applicable law. Check City is a licensed lender in each state where it operates. Loans are intended for short-term financial needs only. Please borrow responsibly.