Learn what your payment to income ratio is, how lenders use it, and why it's a key number for your financial health.

When you apply for a loan, lenders look at a lot of numbers to decide if you qualify. One of the most important numbers they calculate is your payment to income ratio, or PTI. You might not think about this number every day, but it plays a big role in your ability to borrow money. Understanding your PTI can help you see your finances from a lender's point of view. This knowledge can also help you make smarter decisions about taking on new debt.

Your payment to income ratio is a simple but powerful tool. It shows the relationship between your monthly debt payments and your monthly income. Lenders use it to measure your ability to manage new loan payments on top of your existing financial obligations. A lower PTI is generally seen as a sign of financial stability. A higher PTI might signal that your budget is already stretched thin.

This guide will walk you through everything you need to know about your PTI. We will cover how to calculate it, what lenders consider a good ratio, and how it differs from another common metric called debt to income ratio. By the end, you will have a clear picture of this important financial concept. You will also know how to use this information to strengthen your position when you need to borrow.

What is a Payment to Income Ratio?

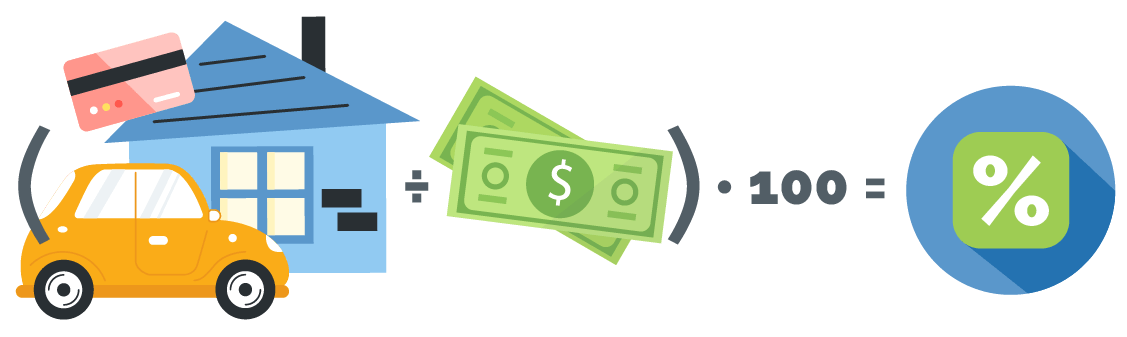

Your payment to income ratio is a percentage. It represents the portion of your gross monthly income that goes toward paying specific debts. These debts typically include things like a proposed new loan payment, along with other major recurring obligations. Common debts included in this calculation are rent or mortgage payments, car loans, student loans, and minimum credit card payments. It does not usually include variable living expenses like groceries or utilities.

To find your PTI, you divide your total monthly debt payments by your total gross monthly income. You then multiply that result by 100 to get a percentage. For example, if your total monthly debt payments are $1,200 and your gross monthly income is $4,000, your PTI would be 30 percent. This means 30 percent of your income is committed to debt repayment before taxes and other deductions are taken out.

Lenders use this calculation to assess risk. They want to be reasonably sure you can afford to pay back a new loan without financial hardship. A lower PTI suggests you have more disposable income available. This makes you a more attractive candidate for a loan. A higher PTI indicates that a large share of your income is already spoken for, which could make managing an additional payment difficult.

It is important to note that different lenders may have different standards for what they include in the "payment" part of the equation. Some may look only at the payment for the loan you are applying for. Others may consider all your recurring debt obligations. Always ask a lender what specific debts they include in their PTI calculation if you are unsure.

How to Calculate Your PTI

Calculating your own payment to income ratio is straightforward. First, gather information on all your monthly debt obligations. Make a list that includes your rent or mortgage, car payment, student loan payment, and the minimum payments on any credit cards or personal loans. Do not include non-debt expenses like insurance, phone bills, or entertainment.

Next, determine your gross monthly income. This is your income before any taxes, Social Security, Medicare, or other deductions are taken out. If you are paid hourly, multiply your hourly wage by the number of hours you work in a typical week, then multiply that by 52 and divide by 12 to get your monthly average. If you have multiple jobs or other sources of income, include the gross amount from all of them.

Now, add up all your monthly debt payments to get a total. Take that total and divide it by your gross monthly income. Finally, multiply that number by 100. The result is your PTI expressed as a percentage. For instance, total monthly debts of $1,500 divided by a gross monthly income of $5,000 equals 0.30. Multiplying by 100 gives you a PTI of 30 percent.

PTI Ratio = (Total Monthly Debt Payments / Gross Monthly Income) x 100

Doing this calculation yourself gives you valuable insight. You can see exactly how much of your income is dedicated to debt. This can be a helpful reality check for your budget. If your PTI is higher than you expected, it might be a signal to focus on paying down existing debt before applying for anything new. Knowing your number puts you in control of the conversation when you speak with a lender.

What is a Good Payment to Income Ratio?

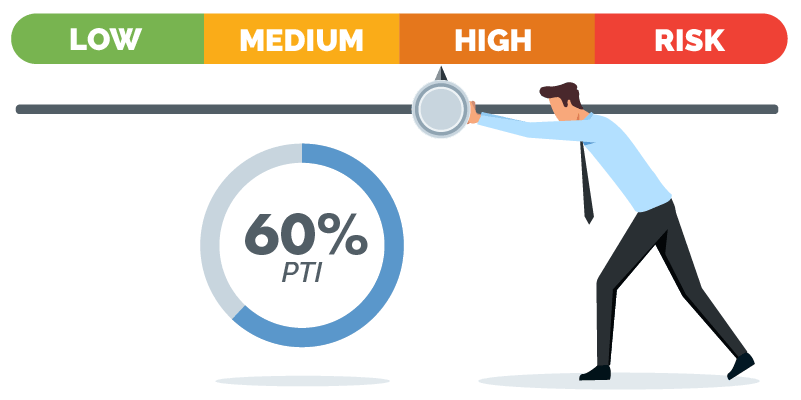

There is no single magic number for a good payment to income ratio. Lending standards can vary. However, many conventional lenders, especially in mortgage lending, often use guidelines set by government-sponsored enterprises. A common benchmark they look for is a PTI of 28 percent or less for just the housing payment. This is known as the front-end ratio.

When lenders consider all your monthly debt obligations, including the proposed new payment, they look at the back-end ratio. A widely accepted standard for this total debt to income ratio is 36 percent or less, though some lenders may accept ratios up to 43 percent or higher in certain cases. It is crucial to understand that a lower ratio is almost always more favorable. It demonstrates greater financial flexibility to a potential lender.

Your specific situation also matters. Lenders may consider other factors like your credit history, savings, and the length of your employment. Someone with a very strong credit score and a long stable job history might be approved with a slightly higher PTI than someone with a newer credit file. The PTI is one important piece of the puzzle, not the only deciding factor.

If your calculated PTI is higher than these general guidelines, do not be discouraged. It simply means you may need to take some steps to improve your financial profile before applying for a major loan. You could work on paying down credit card balances to lower your minimum payments. You could also look for ways to increase your income. Even a small improvement in your PTI can make a difference in how lenders view your application.

PTI vs DTI: What's the Difference?

You will often hear the terms payment to income ratio and debt to income ratio, or DTI, used. While they are related, they are not exactly the same thing. Understanding the distinction is key. Your PTI typically refers to the ratio involving specific, recurring debt payments. As we discussed, this often includes major items like housing, auto loans, and installment loans.

Your debt to income ratio is usually a broader calculation. It may encompass all your monthly debt obligations, including the smaller ones. Some DTI calculations might even include alimony or child support payments. The exact definition can vary by lender. The core idea is that DTI gives a wider view of your total debt burden relative to your income.

For most people, their DTI will be a slightly higher percentage than their PTI. This is because DTI includes more types of debt. When a lender asks for your "debt to income ratio," they are most likely referring to the broader back-end ratio that includes all your minimum monthly debt payments. It is always a good practice to clarify what debts a lender includes in their calculation.

Both ratios are critical tools in the underwriting process. They help lenders standardize how they measure an applicant's ability to repay. By knowing both your PTI and your DTI, you get a complete picture of your debt health. You can identify which debts are having the biggest impact on your ratios. This knowledge allows you to create a targeted plan to pay down debt and improve your numbers over time.

Why Your PTI Matters for Loan Approval

Your payment to income ratio is a direct measure of your cash flow. Lenders are in the business of assessing risk, and your PTI helps them quantify the risk of you not being able to make payments. A high PTI suggests that your budget has little room for error. An unexpected expense or a drop in income could make it hard for you to keep up with all your obligations, including a new loan.

This is why lenders set limits. They want to ensure that you are not overextending yourself. Approving a loan for someone with a very high PTI is risky for the lender. It is also potentially harmful for the borrower, as it could lead to missed payments, late fees, and damage to their credit score. Responsible lending practices involve saying no to applications that would likely cause financial stress.

For you, the borrower, monitoring your PTI is a form of financial self defense. It helps you avoid taking on more debt than you can comfortably handle. Before you apply for any new credit, calculate your PTI with the potential new payment included. Ask yourself if you would still be comfortable with your budget if an unexpected cost arose. If the answer is no, it might be wise to wait.

Remember, loan approval is not just about your PTI. Lenders look at your entire financial profile. This includes your credit score, employment history, and assets. A strong profile in other areas can sometimes offset a PTI that is slightly above ideal guidelines. However, your PTI remains one of the most concrete, numerical ways to demonstrate your repayment capacity.

How to Improve Your Payment to Income Ratio

If your PTI is higher than you would like, there are two main ways to improve it. You can increase your income, or you can decrease your monthly debt payments. Increasing your income might involve asking for a raise, taking on a side job, or finding a higher-paying position. Even a small increase in your monthly earnings can lower your PTI percentage.

The more direct method for most people is to reduce their monthly debt obligations. Focus on paying down high-interest debt first, like credit card balances. As you pay down the principal, your minimum monthly payment will decrease. You could also explore options like debt consolidation. This involves taking out a single new loan to pay off multiple existing debts, ideally with a lower overall monthly payment.

Another strategy is to avoid taking on new debt. Every new loan or credit card increases your monthly obligations and raises your PTI. Before making a major purchase on credit, consider saving up for it instead. This not only keeps your PTI low but also saves you money on interest. It is a powerful habit that contributes to long-term financial stability.

Finally, make a budget and stick to it. A detailed budget helps you see where your money is going. It can reveal opportunities to cut back on discretionary spending. The money you save can then be directed toward paying off debt faster. Improving your PTI is not an overnight process, but with consistent effort, you can lower your ratio and strengthen your financial foundation.

Key Takeaways on Payment to Income Ratio

Your payment to income ratio is a crucial number that lenders use to evaluate your loan applications. It compares your monthly debt payments to your monthly income. A lower PTI generally indicates you are in a better position to handle additional debt. You can calculate your own PTI by dividing your total monthly debt payments by your gross monthly income.

A widely used benchmark for a good total debt to income ratio is 36 percent or less. Remember that PTI and DTI are similar but may be calculated differently by various lenders. Your PTI matters because it shows lenders how much of your income is already committed, which helps them assess risk. If your ratio is high, you can improve it by increasing your income, paying down existing debt, and avoiding new debt.

Understanding this concept empowers you to manage your finances proactively. Before applying for any loan, knowing your PTI helps you gauge your own readiness. It allows you to have more informed conversations with lenders. By keeping this ratio in a healthy range, you not only improve your chances of loan approval but also build a more secure and stable financial life for yourself.

This content is for informational purposes only and does not constitute financial or legal advice. Loan products, terms, amounts, rates, fees, and funding times may vary by state and applicant qualifications. All loans are subject to approval and verification under applicable law. Check City is a licensed lender in each state where it operates. Loans are intended for short-term financial needs only. Please borrow responsibly.