A deferred payment is a term used in the credit industry referring to the ability to extend a billing date. You might come across deferments when shopping or using a loan.

A deferred payment can refer to a method of paying for products or services. It can also refer to a loan repayment option that can extend or delay an upcoming payment period. Depending on the situation, this type of payment might also include a credit card.

Deferred payments can be useful when circumstances make it difficult to make payments right now. They can offer financial flexibility that can be exactly what you need. At the same time, deferred payments have some disadvantages. They can be tricky in regards to paying off your balance before the interest kicks in without incurring more fees.

What is a Deferred Payment?

In finance, the word defer is a verb that means to put off, delay, or postpone something. Outside of finance, the verb defer can mean to delegate something to someone else or to submit to someone else’s decision.

When the verb defer is being used as a noun it changes to deferment or deferral, which is the act of putting off, delaying, or postponing. If something can be deferred than it can be described as deferrable.

Deferred Payment Definition:

A deferred payment is a formal agreement that delays or postpones the due date of the customer’s next payment. A customer or loan borrower might apply for deferred payment for many reasons, like financial hardship.

Deferments can apply to many settings like shopping, online payday loans, student loans, or even college semesters. For example, a student might defer a semester by opting to not go to college one semester, with plans to continue their schooling the following semester. A shopper can sometimes purchase an item and defer the payment to a later date so they can buy what they need now and pay later when they’re more able.

Likewise, loan borrowers can sometimes defer payments to make their loan payment at a later date than previously scheduled. A loan deferment might mean that the lender lets you make your payment a week later than normally scheduled.

How Does Loan Deferment Work?

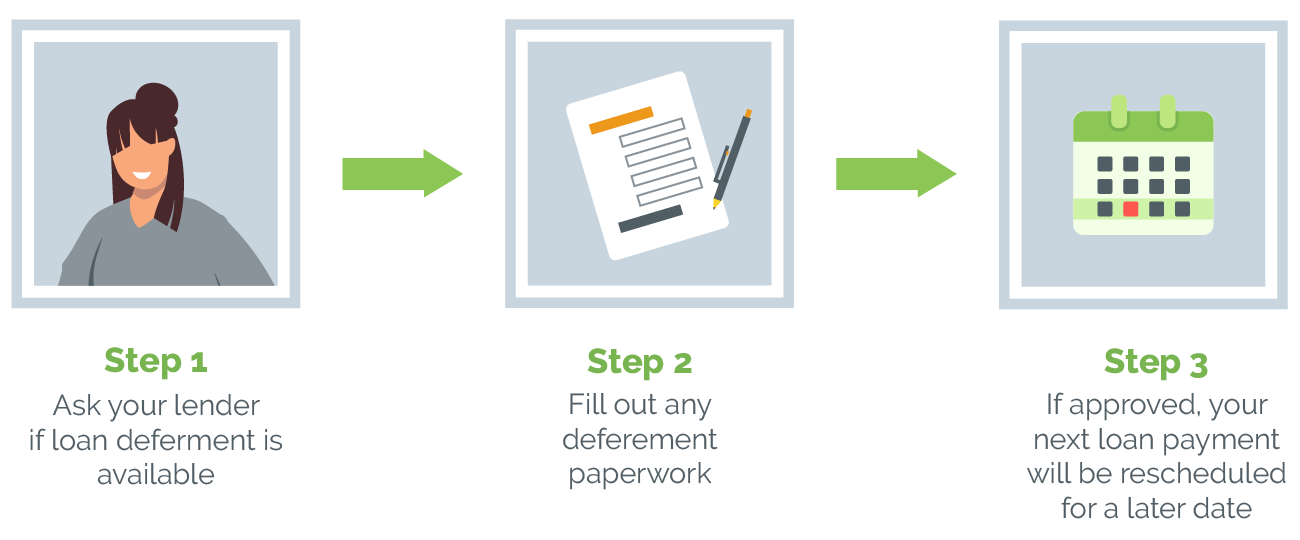

First, you’ll need to find out whether your loan provider offers this option. You will also want to know if you’ll receive a new repayment plan, if specific circumstances like financial hardships are necessary, and the period of time available to defer your payment. Speaking directly with a loan representative is the best way to figure all of this out.

Second, you’ll need to fill out the necessary applications and paperwork to set up the period of time that the payment will be delayed and when the new payment will be scheduled. You may also need to meet certain requirements to qualify like a certain credit score.

Third, if your deferment goes through then you’ll experience a period of time when you won’t have to make payments. Instead, your next loan payment will be rescheduled for a later date and your entire repayment plan will be pushed back however long your deferment period is.

Forbearance vs Deferment

Forbearance and deferments are very similar in that they both allow borrowers to postpone their payments. The main difference is in how interest rates are applied. Other differences might apply depending on the kind of loan and the loan servicer. Normally, neither impact your credit score but they could have long-term effects on your monthly payments and on any unpaid interest.

What is Loan Deferment?

Loan deferments do not accumulate interest during the delayed payment period. A deferment can be seen as a delay on loan payments. After a deferment, the borrower will continue making payments where they left off.

What is Loan Forbearance?

Loan forbearance does accumulate interest during the delayed payment period. A forbearance can be seen as a pause on loan payments. After a forbearance, the borrower will need to make up the payments they missed.

Student Loan Deferment

A student loan deferment lets college students put off repaying their student loans for a certain amount of time. Many student loans are set up to be deferred until the student is no longer in school. Student loan forbearance is another similar option that can help students delay making student loan payments. The options available to students also depend on whether they have federal student loans, federal student aid, or student loans from another service provider. This deferral period might also be contingent on the student being enrolled in at least half-time in classes.

Mortgage Loan Deferment

If you’re having trouble making mortgage payments on your house, then you might qualify for mortgage deferment. This allows the homeowner to postpone their monthly mortgage payments for a given amount of time. This type of program is regulated by the lender itself, so you may need to qualify for this option first. For instance, a lender might say a borrower can defer payments for 12 months.

A mortgage loan deferment is a period of time when your monthly loan repayment obligations are temporarily suspended. In general, no payments are made during the mortgage payment deferment process. When this occurs, interest does not accrue on any outstanding debts.

In Conclusion,

There are many payment options available to loan borrowers and shoppers alike. The choices available to you just depend on the services you use and your personal financial circumstances.

This content is for informational purposes only and does not constitute financial or legal advice. Loan products, terms, amounts, rates, fees, and funding times may vary by state and applicant qualifications. All loans are subject to approval and verification under applicable law. Check City is a licensed lender in each state where it operates. Loans are intended for short-term financial needs only. Please borrow responsibly.