Learn the key differences between traditional and Roth IRAs to make an informed choice about your retirement savings strategy and maximize your financial future.

Planning for retirement can feel overwhelming, but choosing the right Individual Retirement Account (IRA) is one of the most important decisions you can make for your financial future. Two primary options stand out: traditional IRAs and Roth IRAs. Each offers unique tax advantages and features that can significantly impact your retirement savings.

Understanding the differences between these accounts will help you determine which option aligns with your current financial situation and long-term goals. The choice you make today could save you thousands of dollars in taxes and provide greater flexibility in retirement.

What is a Traditional IRA?

A traditional IRA lets you contribute money before paying taxes on it. This means you can deduct your contributions from your taxable income for the year you make them, potentially lowering your tax bill right now.

Your money grows tax-free while it stays in the account. You only pay taxes when you withdraw the funds during retirement. Most people are in a lower tax bracket when they retire, so this setup often saves money in the long run.

How Traditional IRAs Work

Traditional IRAs offer immediate tax benefits that can reduce your current tax burden. When you contribute to a traditional IRA, you may be able to deduct those contributions from your taxable income for the year you make them. This means you pay less in taxes now while building your retirement savings.

Your money grows tax-deferred inside a traditional IRA. You won't pay taxes on investment gains, dividends, or interest until you withdraw the funds during retirement. This allows your investments to compound more effectively over time.

Traditional IRA Tax Benefits

The primary advantage of a traditional IRA is the potential for immediate tax deductions. If you qualify for the full deduction, every dollar you contribute reduces your taxable income dollar for dollar. This can be particularly valuable if you're currently in a higher tax bracket.

However, these tax benefits come with strings attached. You'll pay ordinary income tax on all withdrawals during retirement, including both your original contributions and any investment gains. The tax rate you'll pay depends on your tax bracket at the time of withdrawal.

Required Minimum Distributions

Traditional IRAs require you to start taking Required Minimum Distributions (RMDs) once you reach age 73. The IRS mandates these withdrawals to ensure they eventually collect taxes on the money that has been growing tax-deferred for decades.

The amount of your RMD depends on your account balance and life expectancy. Missing an RMD results in a steep penalty of 50% of the amount you should have withdrawn. This requirement can impact your retirement planning strategy and may force you to take distributions even if you don't need the money.

What is a Roth IRA?

A Roth IRA works the opposite way from a traditional IRA. You contribute money after paying taxes on it, so you do not get an immediate tax deduction. However, your money grows tax-free and you can withdraw it tax-free in retirement.

This arrangement works well if you expect to be in a higher tax bracket when you retire or if tax rates increase over time. You pay taxes at today's rates instead of unknown future rates.

How Roth IRAs Work

Roth IRAs flip the tax equation compared to traditional IRAs. You contribute money that has already been taxed, meaning you don't get an immediate tax deduction. However, this upfront tax payment unlocks powerful long-term benefits.

Once your money is in a Roth IRA, it grows completely tax-free. You'll never pay taxes on qualified withdrawals in retirement, regardless of how much your investments have grown. This can result in substantial tax savings over the long term, especially if you start contributing early in your career.

Roth IRA Tax Advantages

The tax-free growth and withdrawals of Roth IRAs become more valuable the longer your money has to compound. If you contribute $6,000 annually for 30 years and your investments grow at 7% per year, you could have over $600,000 in your account. With a Roth IRA, you could withdraw all of that money tax-free in retirement.

This tax-free status extends to your beneficiaries as well. If you leave a Roth IRA to your children or grandchildren, they can continue to benefit from tax-free growth, making Roth IRAs powerful estate planning tools.

Flexibility and Withdrawal Rules

Roth IRAs offer more flexibility than traditional IRAs when it comes to withdrawals. You can withdraw your original contributions at any time without taxes or penalties since you've already paid taxes on that money. However, earnings withdrawals before age 59½ may be subject to taxes and penalties unless you qualify for specific exceptions.

Unlike traditional IRAs, Roth IRAs don't require minimum distributions during your lifetime. This allows your money to continue growing tax-free for as long as you want, providing more control over your retirement income strategy.

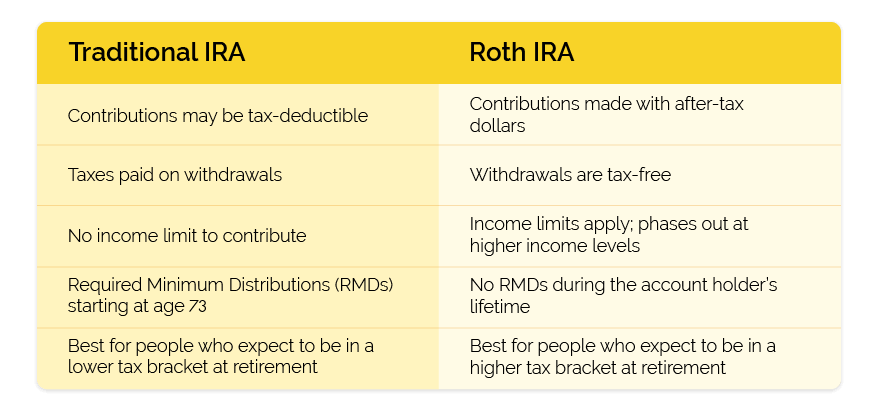

The Key Differences Between Traditional vs Roth IRAs

When planning for retirement, understanding the difference between Traditional IRAs and Roth IRAs can help you choose the account that best fits your financial goals.

A Traditional IRA offers potential upfront tax benefits, making it a good option if you want to lower your taxable income now.

In contrast, a Roth IRA provides tax-free withdrawals in retirement, which can be ideal if you expect to be in a higher tax bracket later. Consider your current income, expected retirement income, and tax situation when deciding which IRA works best for you.

Income Limits and Contribution Rules

Both traditional and Roth IRAs have specific rules governing who can contribute and how much they can contribute. For 2024, the annual contribution limit is $7,000 for individuals under age 50, with an additional $1,000 catch-up contribution allowed for those 50 and older. This number may adjust depending on the tax year.

Traditional IRA Income Considerations

Anyone with earned income can contribute to a traditional IRA, but the tax deductibility of those contributions depends on your income level and whether you have access to a workplace retirement plan. If you're covered by a 401(k) or similar plan at work, the deduction phases out at higher income levels.

For 2024, single filers with workplace retirement plans see their deduction begin to phase out at $77,000 of modified adjusted gross income, completely phasing out at $87,000. Married couples filing jointly face phase-out ranges from $123,000 to $143,000.

Roth IRA Income Restrictions

Roth IRAs have strict income limits that determine eligibility to contribute. High earners may be completely prohibited from making direct Roth IRA contributions.

For 2024, single filers begin to see contribution limits phase out at $138,000, with complete phase-out at $153,000. Married couples filing jointly face phase-out ranges from $218,000 to $228,000.

These income limits make Roth IRAs particularly attractive for younger workers and those earlier in their careers when their incomes may be lower. However, high earners can sometimes use backdoor Roth conversion strategies to fund Roth IRAs indirectly.

Which IRA Type Should You Choose?

Your choice depends on whether you want tax benefits now or tax benefits later. Consider your current tax bracket, expected retirement tax bracket, and how long you have until retirement.

Current vs Future Tax Rates

If you expect to be in a lower tax bracket in retirement than you are now, a traditional IRA might make more sense. The immediate tax deduction provides value at your current higher rate, while you'll pay taxes on withdrawals at your lower retirement rate.

If you expect to be in the same or higher tax bracket in retirement, a Roth IRA could be more beneficial. You pay taxes at today's rates and enjoy tax-free withdrawals when your tax rate might be higher.

Age and Time Horizon Considerations

Younger investors often benefit more from Roth IRAs because they have decades for their investments to grow tax-free. The longer your money has to compound, the more valuable the tax-free growth becomes.

Older investors closer to retirement might prefer the immediate tax benefits of traditional IRAs, especially if they expect their tax rates to decrease in retirement. However, Roth IRAs can still make sense for older investors focused on estate planning.

Diversifying Your Tax Strategy

You don't have to choose just one type of IRA. Many financial experts recommend tax diversification, which means having both traditional and Roth retirement accounts. This strategy provides flexibility in retirement to manage your tax burden by choosing which accounts to withdraw from based on your annual tax situation.

Common Scenarios and Recommendations

Different life situations often point toward one IRA type over the other. Understanding these scenarios can help clarify which option might work for your circumstances.

Early Career Professionals

Young professionals just starting their careers often find Roth IRAs more appealing. They're typically in lower tax brackets, making the lack of immediate tax deduction less painful. Plus, they have decades for tax-free compounding to work its magic.

The flexibility to withdraw contributions without penalties also appeals to younger savers who might need access to their money for major life events like buying a first home or paying for education.

Mid-Career High Earners

Professionals in their peak earning years might benefit more from traditional IRAs if they qualify for the tax deduction. The immediate tax savings can be substantial when you're in higher tax brackets.

However, high earners need to consider income limits for both deductible traditional IRA contributions and direct Roth IRA contributions. Many in this category end up using workplace 401(k) plans as their primary retirement savings vehicle.

Pre-Retirees and Estate Planners

Those nearing retirement have less time to benefit from tax-free compounding, potentially making traditional IRAs more attractive for the immediate tax benefits. However, if estate planning is a priority, Roth IRAs offer advantages since they don't require minimum distributions and provide tax-free inheritance for beneficiaries.

Can You Have Both Types of IRAs?

Yes, you can own both traditional and Roth IRAs at the same time. The annual contribution limits apply to your total contributions across all IRA accounts, not each account separately.

Having both types gives you flexibility in retirement. You can withdraw from traditional accounts when you want to stay in lower tax brackets and use Roth accounts for larger expenses or emergencies.

Some people convert traditional IRA money to Roth accounts over time. This strategy works well if your income drops temporarily or if you want to gradually move money to tax-free status.

Common Mistakes to Avoid

Do not choose an IRA type based only on what others recommend. Your personal tax situation, income level, and retirement timeline create unique factors that affect which option works for you.

Avoid putting all your retirement savings in one account type. Tax diversification helps you adapt to changing tax laws and personal circumstances during retirement.

Do not forget about the 5-year rule for Roth conversions. Money converted from traditional to Roth accounts must stay invested for 5 years before you can withdraw it penalty-free, even if you are over 59.5.

The Bottom Line

Choosing between traditional and Roth IRAs comes down to timing your tax payments. Traditional IRAs work well when you want immediate tax deductions and expect lower retirement tax rates. Roth IRAs make sense when you prefer tax-free retirement income and maximum flexibility.

Consider your current income, expected future income, other retirement accounts, and how long you have until retirement. Many people benefit from having both account types to create tax flexibility in retirement.

The most important step is starting to save for retirement as early as possible. Both traditional and Roth IRAs offer significant advantages over taxable investment accounts, so pick the one that fits your situation and get started today.

This content is for informational purposes only and does not constitute financial or legal advice. Loan products, terms, amounts, rates, fees, and funding times may vary by state and applicant qualifications. All loans are subject to approval and verification under applicable law. Check City is a licensed lender in each state where it operates. Loans are intended for short-term financial needs only. Please borrow responsibly.