Owning a home is an expensive investment. Fortunately, there are helpful tax breaks for homeowners that can help when tax season comes around.

Tax breaks for homeowners can really make a difference. Owning a house comes with a lot of costs, so taking advantage of tax breaks for homeowners wherever you can is wise. By using deductions and credits specifically designed for homeowners, you can lower your tax liability so you can pay less in taxes.

By paying less in taxes you can keep more money for yourself and other household expenses. Tax breaks for homeowners could also help you get a larger tax refund each year. And who doesn't love getting a bigger tax refund check?

There are many qualifications and restrictions you will need to know to use homeowner tax deductions when filing taxes. But once you get the hang of it, you'll be grateful that you did. You'll have more money for your budget, savings accounts, or even home improvements if you wanted!

What are Tax Breaks for Homeowners?

Sometimes the Internal Revenue Service (IRS), who is in charge of handling taxes, will make special exceptions and help for specific demographics of people. For example, there are tax credits for parents, which are made for parents with children, or guardians who take care of dependents at home, like the child tax credit. Deductions that apply specifically to taxpayers who own their house are another example of the IRS trying to lend a little help to taxpayers that may have extra expenses to think about, like childcare expenses or home expenses.

Tax breaks for homeowners are any tax deductions, tax credits, or tax exemptions that are either designed for homeowners, or could apply to homeowners. They help ease tax burdens on people who own their home.

.jpeg)

The Benefit of Tax Breaks for Homeowners

Tax breaks for homeowners can even make owning a home more affordable, because the IRS is trying to take into account that you have property costs to manage throughout the year. You might have to replace parts of your house that are old or pay for repairs after a storm or a flood. Tax breaks for homeowners can help ease the amount of taxes you owe each year so you can have a bigger budget for your home and in essence, reduce the costs of owning a house.

Standard vs Itemized Deductions for Homeowners

What are standard vs itemized deductions for homeowners? Essentially, taxpayers can handle tax deductions in 1 of 2 ways. You can either take a standard deduction or submit an itemized deduction. When it comes to tax breaks for homeowners, the same principle applies.

The Standard Deduction

If you take a standard deduction than there is less math involved for you. Instead of having to look through receipts, list a bunch of different expenses, and figure out which ones qualify as an eligible expense, you can simply take a standard deduction. This will lower your taxable income by a one fixed amount.

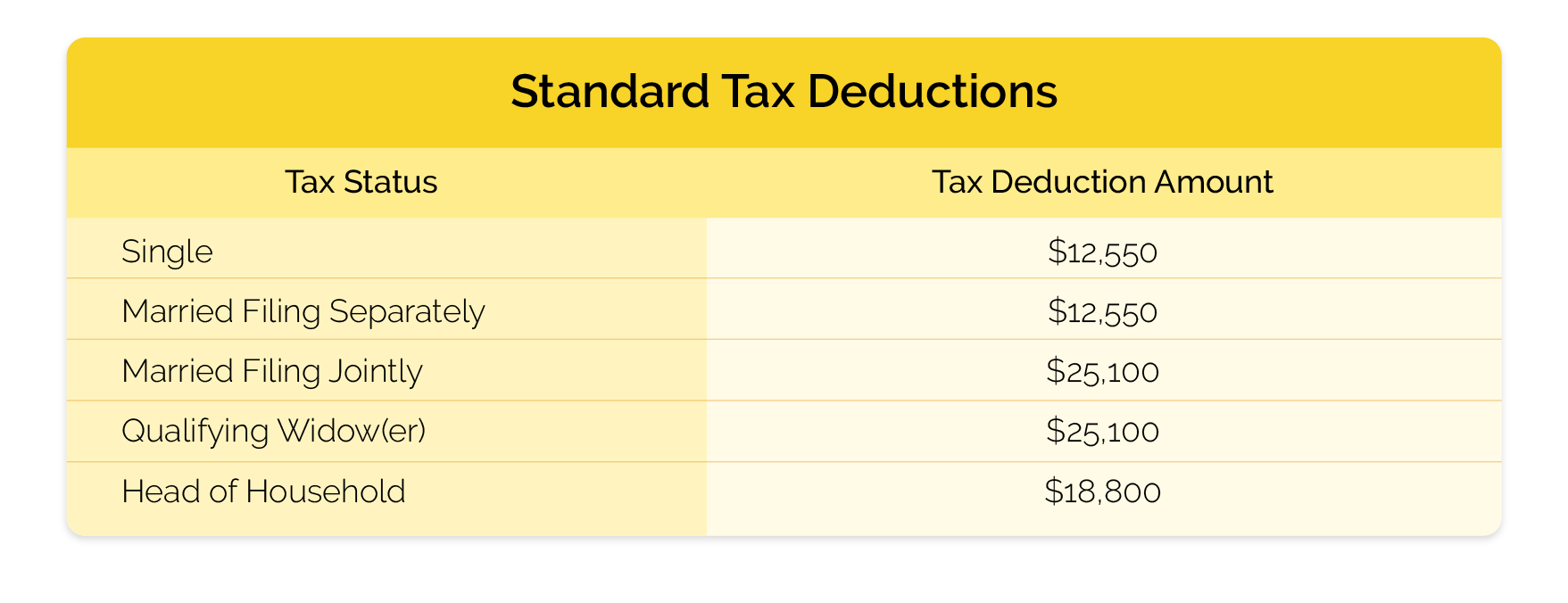

The amount of your standard deduction depends on your current tax status and the tax bracket you fall under. The following are the standard tax deductions available to taxpayers depending on their tax status:

Standard Tax Deductions

The tax deduction amounts listed above go toward your adjusted gross income (AGI). This amount will lower the amount of your total income that is subject to taxes, helping you owe less overall. The standard deduction is also available to everyone, regardless of their situation or whether they would have had no qualifying expenses for itemizing.

The Itemized Deduction

Doing an itemized deduction works similarly to a standard deduction in that, the amount you calculate in your itemization also goes toward reducing your AGI and reducing your overall taxable income. But the method of itemizing adds a few extra steps.

Instead of taking the deduction that goes along with your tax status, you'll need to sit down and go over all your potentially qualifying expenses and list them all out for the IRS. The total amount that gets deducted from your taxable income will then vary per person. But if you've had a lot of qualifying home expenses in the past year, then taking the itemized deduction might be the better choice for you.

Examples of Tax Breaks for Homeowners

There are 8 tax breaks for homeowners available to qualifying taxpayers that could apply to you and your homeowning situation.

- Mortgage Interest Tax Break

- Private Mortgage Insurance (PMI) Premiums

- Discount Points

- Property Taxes

- Mortgage Tax Credit

- Interest on Home Equity Loans

- Home Improvement Expenses

Each one of these tax breaks for homeowners comes with its own restrictions, qualifications, and conditions. These terms and conditions can also sometimes be subject to change, so you'll always want to check with the IRS's official government website for any updates or changes to these available deductions.

.jpeg)

Mortgage Interest Tax Break

Many people take out a mortgage in order to finance their home. These mortgage loans, like most loans, accumulate interest over time. Because of this, mortgage borrowers end up paying for the mortgage loan amount (aka the principal) as well as the interest amount. You may see these 2 kinds of mortgage payments referred to as principal payments and interest payments. Principal payments go toward paying off the principal loan amount and interest payments go toward paying off the additional interest on the loan.

When you make payments toward the interest on a home mortgage, you can deduct those amounts from your taxes as a neat tax break for homeowners! But you can only use this deduction on mortgage debts that are $750,000 or less. For taxpayers who have a "married filing separately" tax status, this amount goes down to $375,000 in mortgage debt.

Interest on Home Equity Loans

What even is a home equity loan? A home equity loan is a type of loan that allows borrowers to use the value of their home to secure a loan. This is similar to how a title loan allows borrowers to use the value of their car to secure a loan.

If you used home equity loan money to pay for qualifying expenses like buying a new home, building a home, or improving your home, then those loan interest payments could be tax deductible.

Mortgage Tax Credit

The mortgage tax credit is a special tax credit designed for low-income and first-time homebuyers. This tax credit was made to help people buying their first home, and people who are in low-income brackets, afford a home a little easier. If you qualify for this program, then you can claim this mortgage tax credit for $2,000 off your tax bill.

Discount Points

Mortgage points can come in the form of origination points or discount points. Origination points are the fees you pay a mortgage lender upon entering a mortgage loan. Discount points aren't fees, but are a way to pay interest upfront by purchasing "points" that then lower your mortgage interest rate.

If you bought discount points to lower your mortgage's interest rate this past tax year, then you could deduct those payments from your taxes.

Private Mortgage Insurance (PMI) Premiums

Do you have mortgage insurance? You may have a required form of mortgage insurance if you paid les than 20% for your home's down payment. Mortgage insurance payments are tax deductible, but only if you AGI isn't greater than $100,000. For married filing separately taxpayers this amount goes down to $50,000.

Property Taxes

State and other local governments often have property taxes on homeowners, landowners, and other real estate owners. The payments you make toward state and local property taxes can be deducted from your taxes. But there is a limit to how much you can deduct. You can deduct up to $10,000 for both state and local property tax payments.

Home Improvement Expenses

Not all home improvement expenses are tax deductible. But some are, specifically any medically necessary improvements to your home, like support bars or wheelchair ramps. Technically, medically necessary home improvement can count as tax deductible medical expenses.

Home Office Expenses

If you are self-employed and use a home office as your principal place of business, then you may be eligible to deduct home office expenses from your taxes. Not everyone qualifies for this tax deduction though. You need to be able to show that your home office is your primary base of professional operations, and not just a regular home office that many people may have in their homes today for occasionally working from home.

.jpeg)

How Do You Get a Tax Break for Buying a House?

The primary way you can get a tax break for buying a house is to use the mortgage tax credit. This is a new homeowner tax credit for first-time homebuyers and low-income home buyers. So you have to meet these low-income or first-time homebuying requirements before you can qualify for this tax credit.

Another tax break for buying a house that could apply to you is if you use a home equity loan to help purchase a new home. The interest payments on a home equity loan that is used for qualifying expenses, like buying a home, can be tax deductible.

Are Home Improvements Tax Deductible?

Home improvements are not always tax deductible. But you can use tax deductions for home improvements if you made home improvements for medically necessary reasons. For example, if you or someone in your household uses a wheelchair, and you make home improvements to add things like support bars and wheelchair ramps, then those expenses could be tax deductible as necessary medical expenses. But making home improvements that aren't medically necessary, like adding another bedroom or making your kitchen bigger, probably won't qualify as tax deductible.

One way to use tax breaks for home improvements is if you use a home equity loan to pay for home improvements and renovations. Then, the interest payments on that loan could be tax deductible.

Is Homeowners Insurance Tax Deductible?

No, homeowners insurance is not tax deductible. But, if you paid less than 20% on your home's down payment, then you probably have a special type of insurance called Private Mortgage Insurance or PMI. This isn't the same as homeowners insurance, but it is a form of insurance associated with owning a home. If you have Private Mortgage Insurance, then those mortgage insurance payments might be tax deductible as a kind of tax break for homeowners.

In Conclusion,

There are so many tax breaks for homeowners available. You'll need to research each one and determine whether they apply to you, because each one comes with its own limits and requirements. Using a tax professional can help with this process a lot because they'll know the most up to date information on available credits and how they might apply to you and your home.

This content is for informational purposes only and does not constitute financial or legal advice. Loan products, terms, amounts, rates, fees, and funding times may vary by state and applicant qualifications. All loans are subject to approval and verification under applicable law. Check City is a licensed lender in each state where it operates. Loans are intended for short-term financial needs only. Please borrow responsibly.