Learn what tax credits and deductions are, how they work, and which expenses may help lower your tax bill.

There are a few ways to reduce tax liability, including tax exemptions, tax deductions, and tax credits. All of these are tax benefits that some people and businesses can qualify to use. Then, each one of these tax benefits can reduce how much you pay in taxes in different ways.

Tax deductions help by reducing the amount of your taxable income. On the other hand, tax credits help by reducing the amount of tax you owe. There is more to know about what tax credits are and how tax credits work, and there are also different kinds of tax credits that could apply to you.

Luckily, you can use experienced tax professionals through the tax services at Check City to make sure you get all the tax credits you might qualify to use. Visit any Check City store with your tax documents, and our friendly tax preparation experts will make sure to get you the best outcome possible for your tax situation.

What is a Tax Credit?

A tax credit is a reduction in taxes owed or an increase in your tax refund. It’s a type of tax benefit offered by the government to individuals or businesses. This tax benefit works by directly reducing the amount of taxes you owe.

When you file taxes each year, the amount of taxes you owe is calculated on your tax return. If you qualify for any tax credits, then the amount of taxes you owe can be reduced.

This kind of tax benefit may be offered by the federal, state, or local government to help out certain groups of people, like businesses, or to incentivize something that is good for the economy or community.

How Do Tax Credits Work?

Tax credits work by directly lowering the amount of taxes you owe. Other tax benefits help you pay less in taxes more indirectly, but tax credits are some of the most direct benefits you can qualify to use.

Because these are applied directly to the amount of taxes you owe, you will first need to calculate what you owe in taxes. This may include calculating tax deductions first so you can get the amount of taxable income you have, and then calculating how much you owe in taxes from the amount of taxable income you have.

The process for an individual to apply tax credits to their tax return might look like this:

Step 1: Determine which tax credits you are eligible to use.

Step 2: On your 1040 tax form, identify and claim the tax credits you wish to apply to your tax return, following the instructions on the form closely to make any necessary calculations.

Step 3: Include supporting documentation like receipts, invoices, forms, or records in your submitted tax return.

For example, a taxpayer might find that they owe $5,000 in taxes, but that they are eligible for a $1,000 tax credit. The credit is subtracted from the amount owed, so that after the credit is applied, the taxpayer owes $4,000 in taxes instead.

Types of Tax Credits

There are 3 different types of tax credits that could help you out this tax season: nonrefundable, refundable, and partially refundable.

These different types of credits could mean that the credit is subtracted from a taxpayer's overall owed taxes, added to a taxpayer's tax refund, or a mix of both.

Nonrefundable Tax Credit

A nonrefundable tax credit is a type of tax credit that reduces the taxes owed to zero but does not result in a tax refund. It's called a nonrefundable tax credit because if the credit is bigger than the amount of taxes owed, then that extra credit is not refunded to the taxpayer in a tax refund. Instead, the taxes owed are just zeroed out.

For example, if a taxpayer owes $5,000 in taxes and their nonrefundable tax credit is $6,000, then this credit reduces their taxes owed to zero, and the surplus credit of $1,000 is not refunded in any way to the taxpayer.

Refundable Tax Credit

A refundable tax credit is a type of tax credit that reduces the taxes owed to zero and results in a tax refund. It's called a refundable tax credit because if the credit is bigger than the amount of taxes owed, then that extra credit is refunded to the taxpayer in a tax refund.

For example, if a taxpayer owes $5,000 in taxes and their refundable tax credit is $6,000, then this credit reduces their taxes owed to zero, and the surplus credit of $1,000 is refunded to the taxpayer.

Partially Refundable Tax Credit

A partially refundable tax credit is a type of tax credit that reduces the taxes owed to zero and refunds a portion of the excess credit. It's called a partially refundable tax credit because if the credit is bigger than the amount of taxes owed, then that extra credit is partially refunded to the taxpayer in a tax refund. But only a portion of that extra credit is refunded.

For example, if a taxpayer owes $5,000 in taxes and their partially refundable tax credit is $6,000, then this credit reduces their taxes owed to zero. A portion of the surplus credit, such as $500, is then refunded to the taxpayer.

Examples of Tax Credits

There are several examples of tax credits that could apply to you and your tax situation, like credits for parents, tax breaks for homeowners, and more.

Child and Dependent Care Credit

The Child and Dependent Care Credit is a tax credit for parents and caregivers that financially helps with child and dependent care costs. This can help taxpayers with childcare expenses and other dependent care expenses

Lifetime Learning Credit

The Lifetime Learning Credit is a tax credit that financially helps taxpayers with educational expenses. This can help taxpayers with expenses from any eligible educational program.

Retirement Savings Contributions Credit

The Retirement Savings Contributions Credit is a tax credit that rewards taxpayers for making contributions to eligible retirement accounts. This can also be called the Saver's Credit. It can help taxpayers who are making contributions to a retirement savings account.

Earned Income Tax Credit

The Earned Income Tax Credit (EITC) is a tax credit designed for taxpaying workers who make a low to moderate income. This can financially help employees who make a low to moderate annual income.

Tax Credit vs Tax Deduction

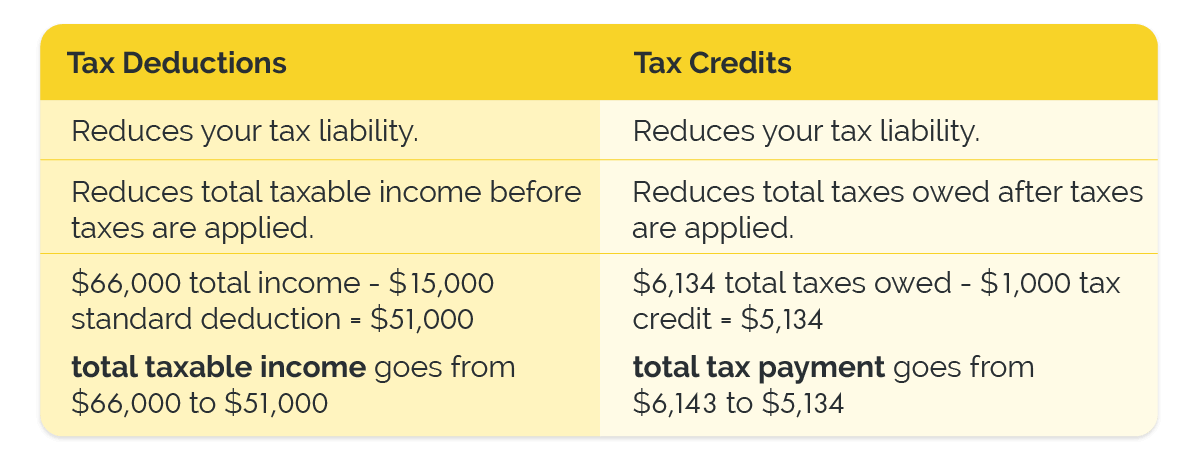

Tax deductions and credits are similar in that they can both help reduce your tax liability, but they’re different in the way they do this.

- Tax deductions lower your tax liability by reducing your total taxable income before taxes are applied. For example, if your total income is $66,000, then a $15,000 standard deduction would reduce your taxable income to $51,000.

- Tax credits lower your tax liability by reducing the total owed after taxes are applied to your overall taxable income. For example, if your total taxes owed are $6,134, then a $1,000 tax credit can reduce your tax payment to $5,134.

What is a Tax Deduction?

A tax deduction is the amount you can subtract (or deduct) from your total income, which then reduces your total taxable income. By lowering how much of your income is taxed, you also reduce the amount of taxes you pay.

Several different types of deductions might apply to you, but the most common types of deductions are standard and itemized deductions.

- The standard deduction is a set amount established by the IRS that can be deducted from your total annual income, reducing the amount of your income that is taxable.

- The itemized deductions are various expenses that are eligible to be deducted from your total annual income, reducing the amount of your income that is taxable.

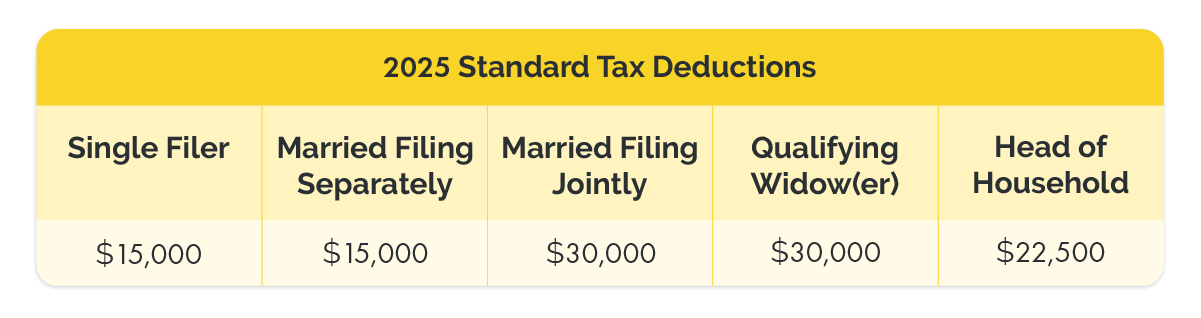

What are the 2025 Standard Deductions?

If you are filing as single or married filing separately, you can deduct $15,000 from your total income. If you’re filing as married filing jointly or a qualifying widow(er), you can deduct $30,000 from your total income. And if you’re a head-of-household filer, you can deduct $22,500 from your total income to get your total taxable income.

- Single Filer: Total Income - $15,000 = Total Taxable Income

- Married Filing Separately: Total Income - $15,000 = Total Taxable Income

- Married Filing Jointly: Total Income - $30,000 = Total Taxable Income

- Qualifying Widow(er): Total Income - $30,000 = Total Taxable Income

- Head of Household: Total Income - $22,500 = Total Taxable Income

How Tax Deductions Work

For a closer comparison, see our guide to standard vs itemized deductions.

Tax deductions work by reducing your taxable income, subtracting deduction amounts (like the standard deduction or several itemized deductions) from your total income. This reduces the amount of your annual income that is taxable.

By reducing the amount of your income that is taxed, the amount you end up paying in taxes is also reduced.

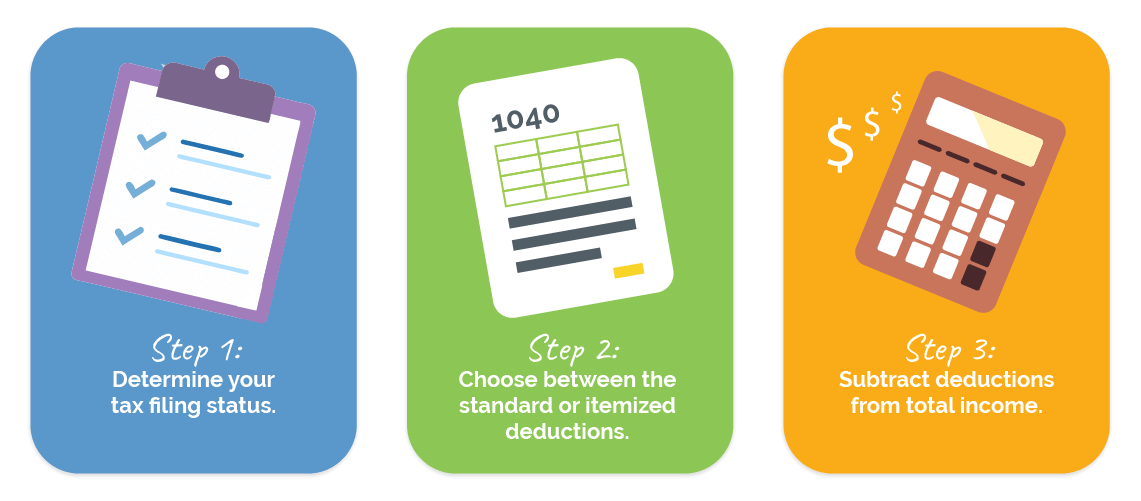

- Determine Your Tax Filing Status. The first thing you need to determine is which tax filing status you will use.

- Choose Between the Standard or Itemized Deductions. Choosing the standard deduction might be simpler, but depending on your eligible expenses, itemizing could result in a larger deduction and a greater reduction in your taxable income.

If you decide to itemize deductions, you’ll have a few extra steps to take. You’ll need to determine which expenses qualify as tax deductions and outline those expenses on your 1040 tax form, or a 1040 schedule form, following the instructions closely.

Also, ensure that you attach any supporting documentation, such as receipts, for these expenses to your submitted tax return.

- Subtract Deductions From Total Income. Once you have your deductions outlined, whether the one standard deduction or several itemized ones, subtract your total deductions from your total income to get your total taxable income.

Total Income - Tax Deductions = Total Taxable Income

Once you have your total taxable income, you can determine which tax brackets apply to you and start calculating how much you’ll pay in taxes for each tax bracket your income falls under.

Read our article about tax brackets to find out which tax brackets apply to you and calculate how much you’ll pay in taxes. You can also learn about your marginal and effective tax rates, as well as other relevant information.

An Example of How Tax Deductions Work

The average US worker earns approximately $66,000 per year ($66,621.80, to be exact). So, if you are a single filer who makes $66k a year, and you decide to use the standard deduction ($15,000 for single filers), then your taxable income would be $51,000.

- Total Income = $66,000

- Standard Deduction = $15,000

- $66,000 - $15,000 = $51,000 total taxable income

If you itemize deductions, this example will include a few more steps. For instance, you’ll add up all your qualifying expenses, provide supporting documentation of these costs in your tax return, and subtract these expenses from your income.

- Total Income = $66,000

- Alimony Payments = $10,000

- Business Use of Your Car = $2,000

- IRA Contributions = $4,000

- Charity Donations = $500

- $10,000 + $2,000 + $4,000 + $500 = $16,500 total itemized deductions

- $66,000 - $16,500 = $49,500 total taxable income

As you can see in this example, the single filer is better off itemizing their deductions since their qualifying expenses can reduce their total taxable income more than the standard deduction.

What Expenses are Deductible?

There are several tax deductions available that can be used alongside the standard tax deduction, while others are only applicable if you choose to itemize your deductions. The types of expenses that qualify may vary depending on the tax year and whether you are filing as an individual.

Individuals can deduct the following expenses alongside the standard deduction:

- Alimony Payments

- Business Vehicle Costs

- Home Business Costs

- IRA Retirement Contributions

- Health Savings Account Contributions

- Early Savings Account Withdrawal Penalty Fees

- Student Loan Interest Payments

- Teacher Expenses

- Work-Related Education Expenses for Some Military, Government, Self-Employed, and People with Disabilities

- Moving Expenses for Military Servicemembers

Individuals can deduct the following expenses if they decide to itemize:

- Bad Debts

- Canceled Home Debts

- Capital Losses

- Donations to Charity

- Gains from Home Sale

- Gambling Losses

- Home Mortgage Interest Payments

- Income, Sales, Real Estate, or Personal Property Tax Payments

- Disasters or Theft Losses

- Medical or Dental Expenses (if they’re over 7.5% of your adjusted gross income)

- Opportunity Zone Investments

- Miscellaneous Itemized Deductions

What Business Expenses Are Deductible?

If you’re filing taxes as a business, there are different requirements your expenses need to meet to qualify as deductible. Businesses especially need to have clear and detailed documentation showing all of the following eligible expenses:

- Energy-Efficient Commercial Buildings Deduction: Includes expenses building owners pay to increase a commercial building's energy efficiency by at least 25% or more.

- Home Office Deduction: Includes expenses that business owners might pay as they use part of their home for business.

- Standard Mileage Rates: These rates cover expenses for the use of vehicles for business purposes.

- Business Interest Deduction: Includes interest payments on certain business expenses.

Make Every Dollar Count This Tax Season

Knowing the difference between tax credits and deductions is key to minimizing your tax liability and keeping more of your hard-earned money. While deductions lower your taxable income, credits reduce the taxes you owe dollar-for-dollar — some even putting money back in your pocket.

As you prepare for tax season, take a moment to review which credits and deductions you qualify for, and keep track of any supporting documentation to maximize your savings. If you need expert guidance to claim every available benefit, our friendly experts at Check City will help you navigate credits, deductions, and all the latest IRS updates so you can file confidently and get the best possible outcome.

This content is for informational purposes only and does not constitute financial or legal advice. Loan products, terms, amounts, rates, fees, and funding times may vary by state and applicant qualifications. All loans are subject to approval and verification under applicable law. Check City is a licensed lender in each state where it operates. Loans are intended for short-term financial needs only. Please borrow responsibly.

Article Sources

“Credits and deductions for individuals,” IRS.gov. August 14, 2024. https://www.irs.gov/credits-and-deductions-for-individuals .

“Credits and deductions for businesses” IRS.gov. November 7, 2024. https://www.irs.gov/credits-deductions/businesses.