Learn how to build an emergency fund, how much you need in emergency savings, and when to use these rainy day funds so you’re prepared for anything.

In all aspects of life, it’s a good idea to always be prepared, including with your personal finances. Unexpected expenses can arise at any time and having an emergency fund set aside for a rainy day can make a huge difference when you need emergency funding.

Learn what an emergency fund is and how to build a fund that can help protect you financially when sudden expenses arise. Whether you're just starting to prioritize your financial security or seeking to enhance your existing safety net, understanding the ins and outs of rainy day funds is essential for safeguarding your financial future.

What is an Emergency Fund?

An emergency fund is a reserve of money set aside for emergency or unexpected expenses. It can also be referred to as a rainy day fund, emergency savings, or a financial safety net.

The purpose of an emergency fund is to provide a financial cushion when life happens and unexpected costs arise. You can rely on these savings if you suddenly lose your job, if you get injured or sick, or if your car or home suddenly needs repairs.

Give yourself the gift of increased financial stability by building your own emergency savings for improved financial peace of mind.

Why Do I Need an Emergency Fund?

You need an emergency fund to protect you in case of a financial setback. Unexpected emergencies can cost a lot of money, like job loss, injury, illness, cars breaking down, natural disasters, and more.

If you aren’t financially prepared for the unexpected, then these instances can put you in greater debt or eat up your savings for other money goals. Having some emergency money set aside can keep sudden expenses from impacting your finances too drastically.

Protect yourself financially by setting aside an emergency savings fund in case of emergencies.

How Much Do I Need in an Emergency Fund?

If you’re going to build up a reserve fund, then you’ll need to know how much you should have in an emergency fund. How much you need in an emergency fund depends on your financial situation and what kind of expenses you’d like to prepare for.

- Consider your financial situation

- Consider the kind of expenses you want to prepare for

In general, your emergency fund amount should equal at least 3 months of expenses. Some experts advise you to stash away 6 months of expenses. Other experts, like the Dave Ramsey emergency fund method, advise you to set aside $1,000 as backup money and then focus on repaying all your debts before building a bigger rainy day fund.

- Set aside at least 3 months’ worth of necessary expenses

- Set aside 6 months’ worth of necessary expenses

- Set aside $1,000 and then repay all debts

A determining factor you might consider in how much you need to put aside is what expenses you want to save up for. For example, emergency funds for rent will need to be worth a few months of your current rent. But a student emergency fund might need to focus on saving up for groceries, gas, or a plane ticket home.

Emergency Fund Calculations

Calculate the amount of money you need in this fund by taking your total monthly necessary expenses and multiplying that number by 3 months.

Total Monthly Expenses x 3 Months = Emergency Fund Amount

$1,000 x 3 = $3,000

Emergency Fund Examples

If your monthly budget includes $1,000 of necessary expenses, then try to eventually put aside $3,000 in emergency savings. You could save up this amount in 1 year by putting aside $250 each month.

If your monthly budget includes $1,500 of necessary expenses, then try to eventually put aside $4,500 in emergency savings. You could save up this amount in 1 year by putting aside $375 each month.

Emergency Fund Ratio

An emergency fund ratio refers to the amount of emergency money a person has saved up compared to how much they spend or make each month. This can also be referred to as a liquid assets ratio because the money you have set aside is considered a liquid asset, ready to cover financial emergencies now.

Emergency Fund / Monthly Expenses or Monthly Income = Emergency Fund Ratio

$3,000 / $1,000 = 3

This ratio number shows how many months your savings can cover if needed. In this example, the person has saved enough to cover them for 3 months. Use this formula to check how many months your current savings can cover in case of an emergency.

How to Build an Emergency Fund

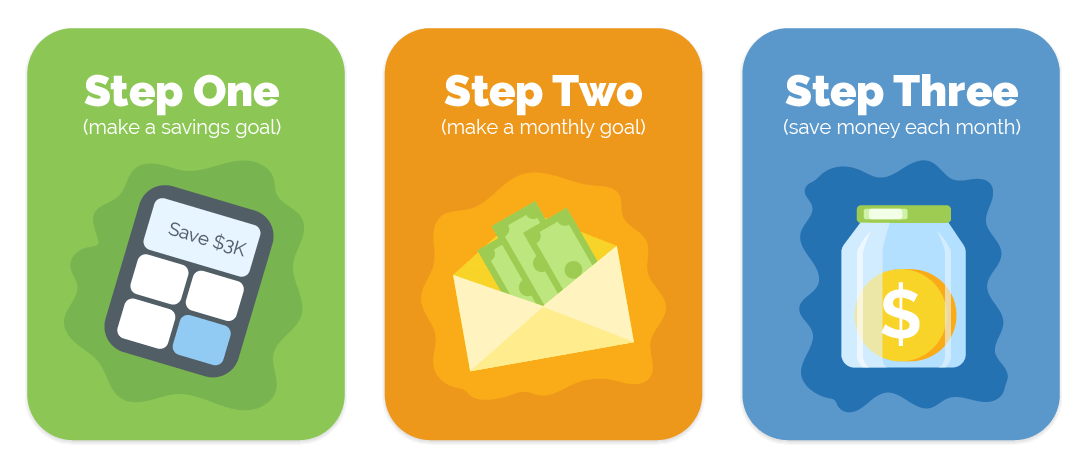

To build an emergency fund, start by calculating your first savings goal for this fund. Then, calculate how much you need to save each month in a certain time frame to reach this goal. Once you reach your first savings goal, you can then continue saving to build an even stronger fund.

Step 1: Make a Savings Goal. Calculate the first savings goal you’d like to reach.

Step 2: Make a Monthly Goal. Calculate how much you need to save each month to reach your savings goal in a certain amount of time.

Step 3: Save Money Each Month. Put aside money each month until you reach your first savings goal. Then, continue saving what you can to build an even stronger emergency cache.

For example, if you spend $2,000 a month on necessary expenses and would like to start by saving up 3 months' worth of emergency funds, then multiply $2,000 by 3 months to get your final savings goal of $6,000. Then divide $6,000 by 12 months to see that you’ll need to put aside $500 each month to reach this goal in 1 year. Or, divide $6,000 by 24 months to see that you’ll need to put aside $250 each month to reach this goal in 2 years.

Another way to build an emergency fund is to start by calculating how much you can put away per paycheck or each month into a savings account for emergencies. Then you can use the emergency fund ratio calculation to regularly check how many months your emergency stockpile of money can cover.

Step 1: Calculate your necessary monthly expenses

Step 2: Calculate how much you have left after necessary expenses

Step 3: Calculate how much you can put aside each month

For example, if you make $2,000 a month and $1,500 goes to necessary expenses, then you potentially have about $500 you could set aside for a rainy day each month.

Where to Put Your Emergency Fund

Where you put your emergency fund is important for making sure your savings are not accidentally used for nonemergencies.

For example, keeping your savings in the same checking account you use for everyday purchases is an easy way to accidentally deplete the money you have set aside for emergencies only.

It’s a good idea to put this money away somewhere safe and separate. Many people put their emergency savings in a separate checking or savings account with your bank or credit union. But you could also put money into a prepaid card or take out cash to keep in a safe at home.

- Checking account

- Savings account

- Prepaid card

- Cash

It’s a smart idea to put money into a high-yield savings account where it can grow, like a certificate of deposit (CD). But you want to be able to access this money in an emergency and some accounts, like a CD, don’t allow users to withdraw money whenever they need to.

So, it’s best to put this money away in a regular savings account or a separate checking account so you can easily access these funds if you need to. A separate checking account or a prepaid card are great places for this amount of money because they come with a debit card you can easily use to cover the costs of an emergency.

When to Use Your Emergency Fund

It can take a long time to build your emergency fund. That’s why you want to make sure you are only using it for real emergencies and not using this money unnecessarily.

Make a financial plan with guidelines for what constitutes an emergency for you and your family members. For example, you might include home repairs as an approved emergency expense, while other households might want to primarily use this money for emergency medical expenses.

An emergency fund should be used for:

- Home repairs

- Medical bills

- Car repairs

- Expenses after a job loss

- Family emergencies

- Legal expenses

- Recovery after a natural disaster

An emergency fund should not be used for:

- Luxury expenses

- Routine expenses

- Debt repayment

- Investments

- Entertainment

- Vacations

Make a list of possible expenses this account is allowed to cover under your financial plans. It might also be smart to create separate bank accounts for different expenses you might want to save for. For example, you might want a savings account for emergency expenses and a separate savings account for home or car expenses.

Avoid using this fund for debt repayments and instead create a separate sinking fund to help tackle your debt repayment plan.

How to Maintain an Emergency Fund

Maintain an emergency fund by continuously putting money into your account, replenishing funds after you use them, and knowing when an emergency fund should not be used. Setting up automated payments into this savings account is also a great way to keep this account well-supplied without having to think about it too much.

- Set guidelines for approved and non-approved expenses

- Set up automated payments into the account

- Continuously add to this account, even after reaching your goal amounts

- Monitor and adjust amounts as financial situations change

The bottom line is to keep this account well stocked and easily accessible so you’re prepared in case of an unexpected financial situation.

This content is for informational purposes only and does not constitute financial or legal advice. Loan products, terms, amounts, rates, fees, and funding times may vary by state and applicant qualifications. All loans are subject to approval and verification under applicable law. Check City is a licensed lender in each state where it operates. Loans are intended for short-term financial needs only. Please borrow responsibly.