Annuities can be a helpful financial tool for retirement. They can create regular income payments in your retirement years and defer year-end taxes as you grow your annuity balance.

Annuity is money paid out in small routine payments typically paid after retirement. There are different types of annuity such as fixed annuity, immediate annuity, variable annuity, and deferred annuity.

Are you thinking about starting an annuity account? Before you do, make sure you understand how an annuity works. This article will help you learn more about annuities, what they can do for you, and help you decide on an annuity type that best fits your personal needs.

The above article is an opinion and is for information purposes only. It is not intended to be investment advice. Seek a duly licensed professional for investment advice.

What is an Annuity?

The word "annuity" means "series of payments." Annuities are a type of fund often created through a contract with your insurance. Annuities are a fund created to be paid back to you, usually at a later date. Annuities are often set up for retirement.

Annuities are usually set up in the following way: you make regular payments into the annuity account, the balance in the annuity can grow tax-free, and then at the time you've specified in your annuity contract, payments from that annuity will get paid back to you in installments, like an allowance.

An annuity is different from a 401K because when you receive your annuity payments back, they are subject to income tax.

How Do Annuities Work?

Basically, an annuity is a funding account designed to set up regular payments for yourself.

When setting up an annuity you'll have to set up what type of annuity you want, how long you want to let the annuity accumulate and grow, when you want to start receiving your annuity funds back in payments, how regularly you want to receive those payments, and how much you want those payments to be.

Annuities can provide a stream of income in your retirement years and can sometimes offer higher returns than the funds you originally put in. Every insurance company will have its own practices for how they handle annuities. Make sure you speak with a provider to thoroughly understand the annuity contracts they offer.

Types of Annuity

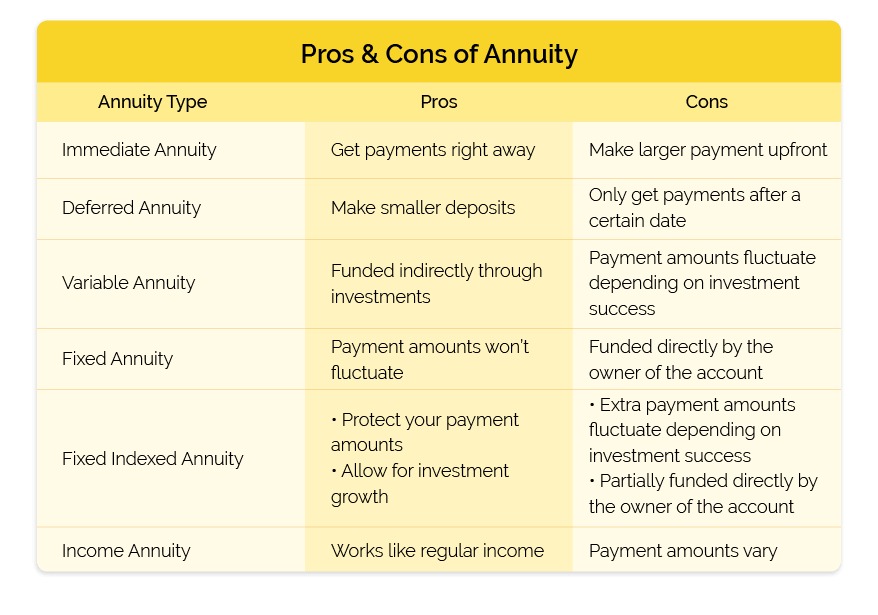

Immediate Annuity

Many annuities are set up so you can only start receiving funds after a certain age or after you've retired. But immediate annuities are set up so you can start receiving payments right away.

An immediate annuity can also be called an immediate payment annuity, a single-premium immediate annuity (SPIA), or an income annuity. It is a type of annuity that guarantees income to the annuitant almost immediately.

Immediate annuities are created when an annuitant pays a lump sum into the annuity all at once. Then those funds become available in regular repayments to the annuitant sooner because they didn't have to wait for the annuity balance to grow.

Deferred Annuity

A deferred annuity is the most common type of annuity. Deferred means that this annuity is set up to start making payments to you only after a certain date in the future.

When you start receiving payments, how long you receive payments, and how much you receive in each payment are all things you determine in your annuity contract.

Delaying payments in a deferred annuity plan helps you make smaller deposits to grow your annuity funds over time. Your annuity funds are also not subject to income tax so long as they remain in the account.

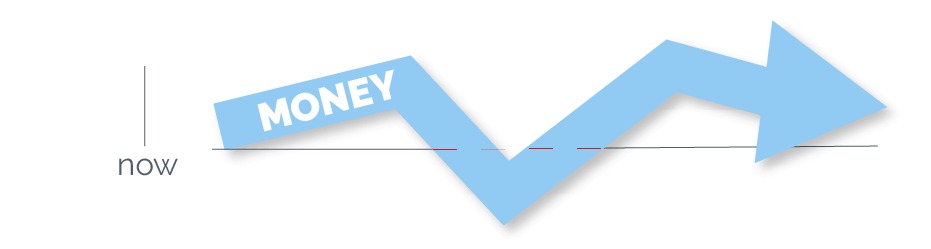

Variable Annuity

Variable annuities allow you to fund your annuity balance through investments. Then, the annuity pays you back depending on how well those investments do.

The risk with variable annuities is that if your investments do poorly, your payments might be lower. But if your investments do well, then a variable annuity can pay better than a fixed annuity.

Fixed Annuity

A fixed annuity is not based on the annuity owner's investment portfolio. Instead, a fixed annuity is funded directly by the owner. Then, a fixed annuity will give the owner fixed payments that don't fluctuate the way an account based on investments might.

Fixed annuities usually have an accumulation phase when the annuity owner is putting money into the account. Then the annuity has a surrender period when the insurance company will pay back the annuity balance to the owner in regular installments.

With a fixed annuity, these payment amounts are guaranteed to stay the same.

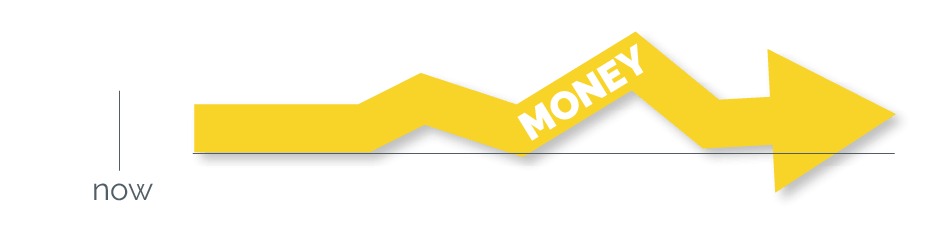

Fixed Index Annuity

A fixed index annuity is like a combination of variable and fixed annuities. A portion of the annuity balance is based on the performance of your investments. But a fixed index annuity will help protect your payments if the market goes down.

A fixed index annuity provides the best of both worlds: guaranteed protection for your payments, but allows for potential growth.

Income Annuity

An income annuity is a type of immediate annuity. As soon as someone takes out the annuity they start receiving payments from it, but the amount of each payment might vary.

Income annuities are called income annuities because they are designed to act as regular income and are often used to fund someone during their retirement years.

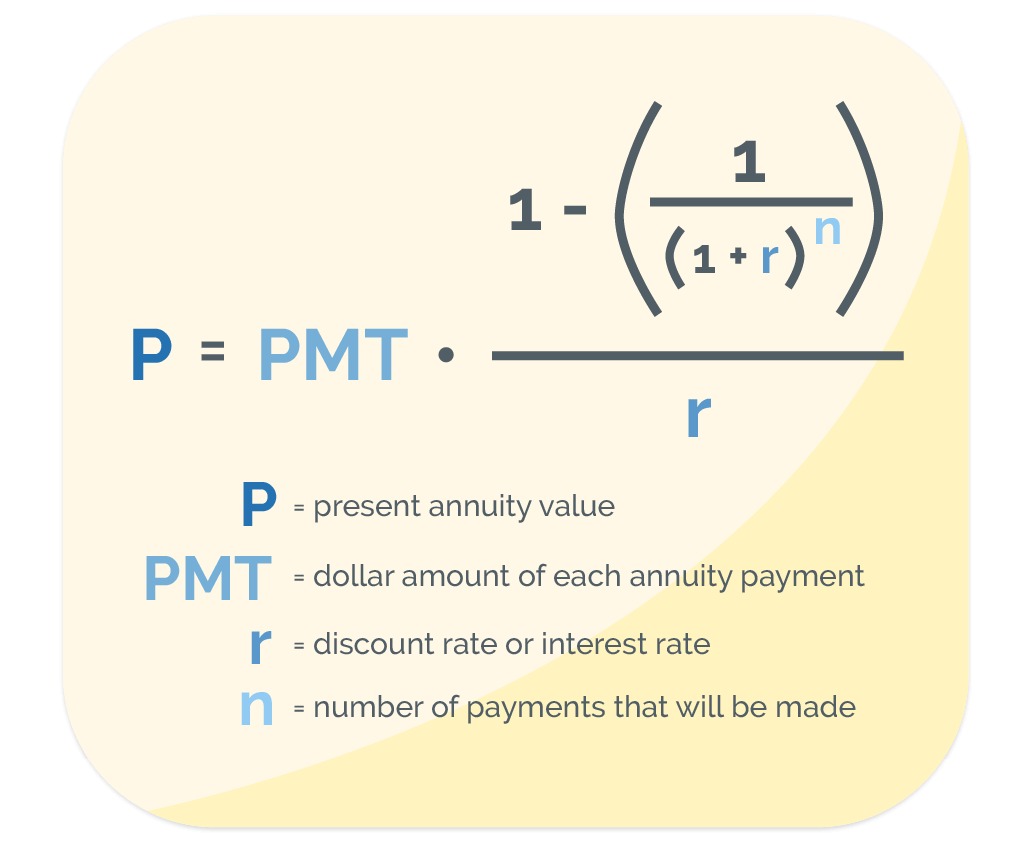

Present Value of Annuity

The present value of annuity refers to how much funds are needed at the present time to fund future payments. The present value of annuity takes into account the change in money's value over time and helps you see which will yield higher returns for you, taking out a lump sum right now, or spreading out your withdrawals in regular payments over time.

Pros and Cons of Annuity

Annuity Formula

There are several complex annuity formulas you can use to help you figure out parts of your annuity.

With annuity formulas you can find the future value of your annuity payments, the present or current value of it, the periodic payments when the present value is known, the periodic payments when the future value is known, the number of payment periods when present value is known, and the number of payment periods when the future value is known.

Annuity Rates

Multi-year guaranteed annuities (MYGAs) are fixed annuities with a guaranteed interest rate. MYGAs are usually set up for 1 to 10 years.

Annuity.org is a great place to research the best annuity rates because they fact-check their information and they update their rates table frequently.

Annuity Loans

Your annuity contract has monetary value. With an annuity loan, you can access the monetary value of your annuity contract to secure loan funding. By using an annuity loan, you can get money from your annuity account without having to actually open and use the account.

This content is for informational purposes only and does not constitute financial or legal advice. Loan products, terms, amounts, rates, fees, and funding times may vary by state and applicant qualifications. All loans are subject to approval and verification under applicable law. Check City is a licensed lender in each state where it operates. Loans are intended for short-term financial needs only. Please borrow responsibly.