Learn all about loan amortization, what it means, and how it works, so you understand the process for loans and assets.

TLDR: Loan amortization is the processing of spreading out loan payments over time, splitting each payment between interest and principal. Early monthly payments are applied toward interest, while later payments reduce the primary balance. Understanding how loan amortization works helps you plan ahead and avoid surprises.

Have you ever taken out a loan for a car, home, or college tuition? If so, you’re probably already somewhat familiar with loan amortization — the process of repaying the amount you borrowed (principal) and interest (the cost of borrowing) during a set period of time. Initially, a significant portion of your payment is allocated to interest, and over time, a greater proportion is applied to the principal.

When you understand loan amortization, you can see how your balance decreases over time, allowing you to create a plan to pay off your loan faster.

What is Amortization?

Loan amortization is the process of spreading out loan payments over time through regular, scheduled payments. Amortized loans, such as mortgages, auto loans, student loans, and personal loans, involve regular payments that help pay off a portion of the loan principal and accrued interest with each payment.

This term can be used in calculations related to loans and loan payments, as well as the expenses of intangible assets. It considers several variables to calculate payments and their relationship to the interest rate, principal balance, and principal payments.

The amortization process ensures the loan is paid off, including the principal and any accrued interest, by the end of the loan term. The schedule provides borrowers with a clear loan repayment plan to achieve the goal of full repayment over time.

For example, let’s say you have a $10,000 loan paid over 3 years at a fixed interest rate. Each monthly payment is applied to both the interest and principal. Early payments mainly cover interest, while later payments knock down the principal amount. By the end of three years, your loan is fully paid off.

How Do Amortizing Loans Work?

Instead of paying off a loan all at once, an amortized loan spreads out the repayment of both the principal and interest over a set period of time. Using a repayment schedule like this can make it easier for borrowers to pay back their loans.

The amortization process works by creating a schedule of regular (often monthly) payments that will repay the entire loan over a specified period of time. Each payment will serve to pay off a portion of the loan's principal and interest. Depending on the loan's schedule, payments at the beginning might include more of the loan's principal or interest to pay off that part of the loan first.

By the end of the amortization schedule, the entire loan, including the principal and interest, will be fully repaid.

Amortizing loans can either have a fixed rate or a variable rate:

- Fixed-rate amortized loans: Your payment stays the same throughout the loan term, but the portion going toward interest decreases over time, while more goes to the principal.

- Variable-rate amortized loans: Your payment may change if interest rates fluctuate, meaning your principal and interest payments can vary from month to month.

The Steps of the Amortization Process

Here’s a simple breakdown of how the amortization process works with each payment:

- Loan amount is disbursed: You receive the loan funds (the principal) from your lender.

- Monthly payment is calculated: The lender sets a fixed or variable monthly payment based on the loan amount, interest rate, and loan term.

- Interest is applied: For each payment, interest is first calculated on the remaining principal balance.

- Remaining payment reduces principal: After interest is paid, the remaining payment is applied toward reducing the loan balance.

This cycle repeats each month until the loan is fully paid off.

What is an Amortization Schedule?

An amortization schedule is a table or chart that outlines each loan payment, showing how much of that payment is applied to the loan's principal (the amount you borrowed) and how much goes toward interest (the cost of borrowing) and accrued interest. An amortization table gives a clear picture of all the numbers related to the loan payment and is helpful for tracking progress, budgeting, and calculating interest savings.

Here’s how to read an amortization table:

- Find the payment date: Each row typically represents a single payment.

- Check the interest portion: See how much of the payment goes toward interest.

- Check the principal portion: See how much reduces your loan balance.

- Note the new balance: Know the amount you still owe after making the payment.

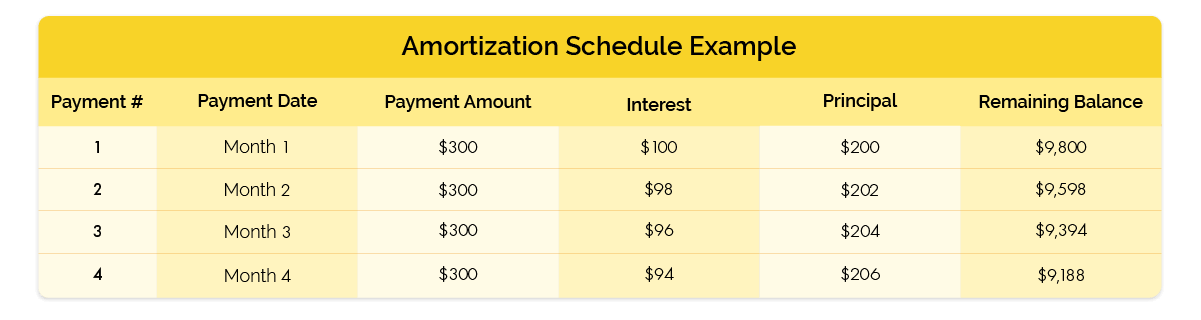

Loan Amortization Examples

Loan amortization works differently depending on the type of loan. Here are a few examples to show how payments are applied to principal and interest over time.

*The following example charts are for illustrative purposes only and do not reflect the amortization schedule of an actual loan.

General Loan

For a $10,000 loan over 3 years, the first payment may be mostly interest, while later payments will include a higher proportion of principal. By following the schedule, you can clearly see your loan balance shrinking month by month.

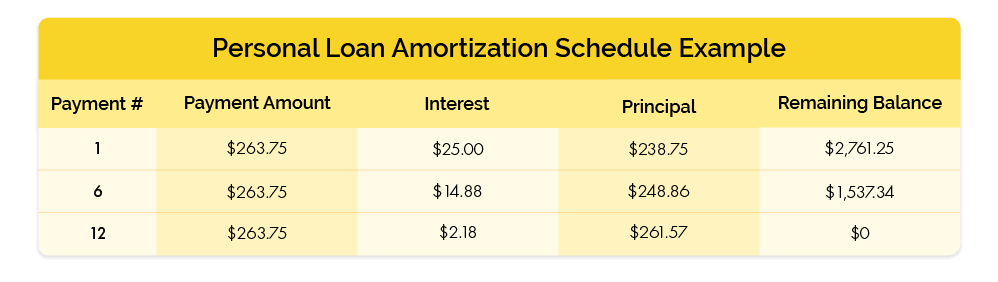

Personal Loans

Personal loans usually have shorter terms and higher monthly payments, which means the loan balance is paid down fairly quickly.

For example, let’s say you have a $3,000 loan with a 10% APR over 12 months. Here’s what the loan amortization schedule might look like:

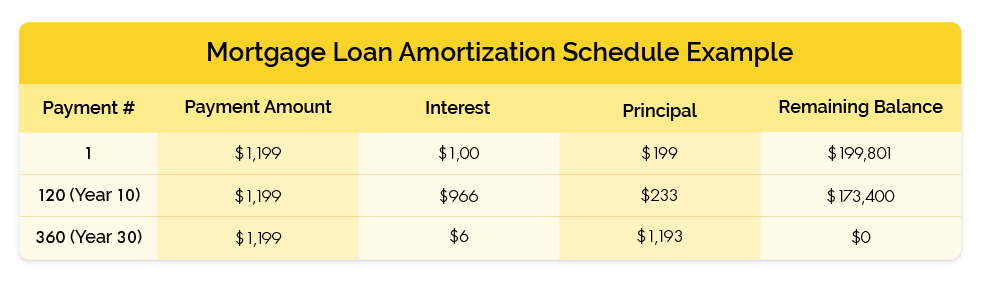

Mortgage Loans

Mortgage loans are long-term loans, often stretching 15 to 30 years. With a mortgage loan, early payments go toward the interest, while the later payments go toward lowering your principal.

For example, let’s say you have a $200,000 mortgage loan at 6% over 30 years. Here’s what you can expect over time.

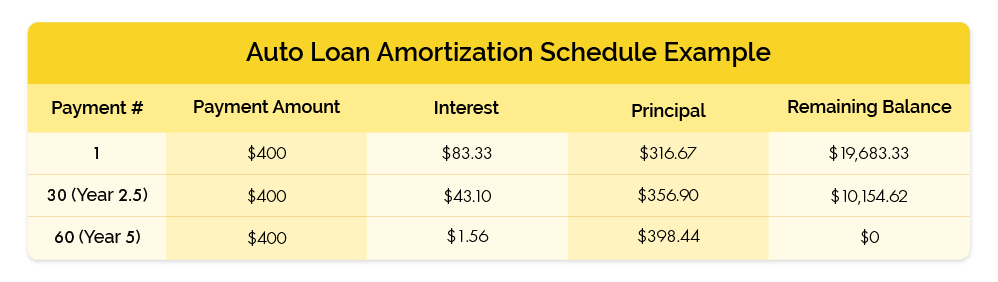

Auto Loans

Auto loans are short-term loans, typically spanning 3 to 7 years. Auto loans tend to have a faster shift toward the principal compared to mortgage loans, accruing less interest over time, but with higher monthly car payments.

Say you have a $20,000 auto loan at 5% APR over five years with a monthly payment of $400. Here’s what you can expect to see over time.

How to Calculate Loan Amortization

Loan amortization shows how your payments are split over time. Here’s a simple formula to calculate your monthly payment:

Payment = P x [r(1 + r)^n] / [(1 + r)^n - 1]

P = Principal (the total loan amount)

r = Monthly interest rate (annual interest/12)

n = Total number of monthly payments

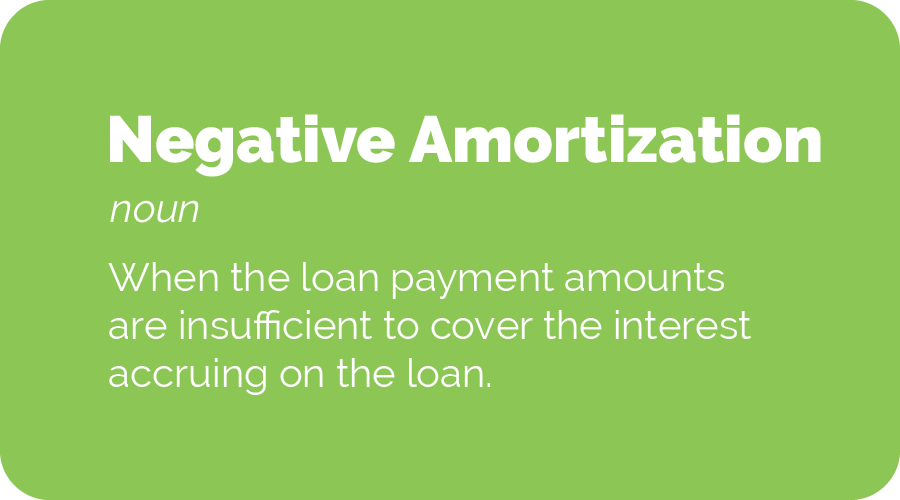

What is Negative Amortization?

Negative amortization occurs when the loan payment amounts are insufficient to cover the interest accruing on the loan. This can then cause the loan's outstanding balance to increase over time, rather than decrease.

Some loans let you make smaller loan payments due to mitigating circumstances. This can include making monthly payments that are too small to decrease your outstanding balance. However, eventually, larger payments will be required to reduce the outstanding balance and ultimately pay off the loan.

Common Negative Amortization Scenarios

Negative loan amortization doesn’t occur with every loan, but there are a few situations to keep in mind:

Adjustable-Rate Mortgages (ARMs)

Some ARMS have a payment cap, which limits how much your monthly payment can rise, even if your interest rate changes. If your capped payment isn’t enough to cover the interest, then the unpaid interest will be added to your loan balance. Over time, this can cause your loan balance to grow, making it more challenging to pay off your debt.

Student Loans with Deferred Interest

Most student loans let you defer payments while you’re in school or experiencing financial hardship. However, interest may continue to accrue during this time. If it isn’t paid, it gets added to your principal balance and increases the total amount you owe.

Risks of Negative Amortization

The most common risks of negative amortization are higher debt, paying interest on interest, and payment shock. The best way to avoid negative amortization is to:

- Know your loan terms and understand deferred interest, adjustable rates, and payment caps.

- Always make at least the interest payment each month.

- Put more toward the principal balance whenever possible.

Being proactive in understanding how negative amortization works can help you manage your loan effectively, avoid unexpected increases in your balance, and pay off your debt on time.

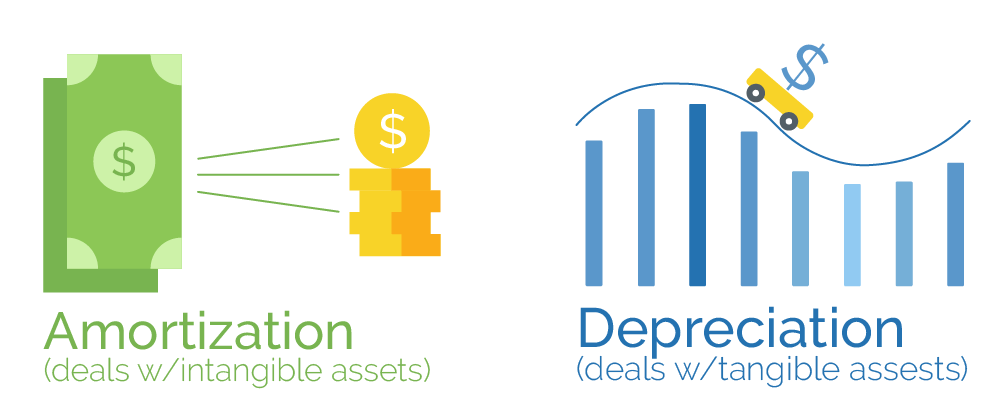

Amortization vs Depreciation

Amortization and depreciation differ in that they are applied to distinct types of assets and serve distinct accounting purposes. Amortization affects your loan balance while depreciation affects the value of your asset. Simply put, amortization affects the amount you owe, while depreciation affects the value of your asset over time.

Benefits of Understanding Loan Amortization

Understanding how loan amortization works provides multiple benefits, giving you more control over your finances. These include:

- Better financial planning: Know exactly how much you owe and when you’ll be debt-free so that you can make a game plan.

- Easier loan comparisons: Focus on the total interest paid, not just the monthly payments, to make smarter borrowing decisions.

- Interest savings: Make extra principal payments early to reduce the total interest you pay and get your loan paid off faster.

- Avoid surprises: Understand how missed or late payments affect your balance, so you’re never caught off guard.

The Takeaway

Loan amortization may seem complicated at first, but knowing how loan amortization works can give you better clarity. Understanding how principal and interest break down your payments, you can make a plan to stay on track to pay off your debt.

Need flexible funding? At Check City, we offer a range of loan options to provide you with the funds you need when you need them.

FAQs About Loan Amortization

What Does Amortization Mean for My Monthly Payments?

Loan amortization means your monthly payment covers both interest and principal. At the early stages of your loan, you’ll make payments toward the interest, while later payments will go toward minimizing your principal balance.

Does Amortization Change If I Make Extra Payments?

Yes, extra payments can reduce interest paid over time and shorten your loan term.

Is Amortization Good or Bad for Borrowers?

Amortization is reasonable when you can afford your monthly payments and if the loan terms are clear. If not, negative amortization is more likely to occur.

Can I Avoid Paying Too Much Interest Early On?

Yes. By making extra payments toward the principal balance, you can reduce your accrued interest and work toward getting out of debt much faster.

Need flexible funding? Check out our installment loans today!

Key Takeaways

- Early payments focus on interest: Most loans start with higher interest payments, while later payments are applied toward the principal.

- Avoid negative amortization: Paying less than the interest due can hurt your loan balance and hinder your progress.

- Extra payments help you save: Paying more toward your principal can save you on interest and help you reach your goals faster.

- An amortization schedule guides your budget: Knowing your repayment schedule makes it easier to budget and compare loans.

This content is for informational purposes only and does not constitute financial or legal advice. Loan products, terms, amounts, rates, fees, and funding times may vary by state and applicant qualifications. All loans are subject to approval and verification under applicable law. Check City is a licensed lender in each state where it operates. Loans are intended for short-term financial needs only. Please borrow responsibly.