Learn about all the different types of interest rates and how they work, including fixed, variable, compound, and simple rates.

When it comes to borrowing, saving, or investing, interest rates play a key role in how much you pay (or earn) over time. But not all interest rates are the same. There are several types of interest rates and they all work differently from each other. Understanding the difference between them can help you make smarter financial decisions.

In this article, we’ll walk you through the most common types of interest rates, how each one works, and where you’re most likely to encounter them.

Fixed Interest Rates

A fixed interest rate is a type of interest rate that stays the same throughout the life of the loan. The interest rate on your loan is not linked to any benchmark or index but is instead decided upon when entering the fixed-rate loan contract.

Fixed-rate payments also stay the same throughout the life of the loan. Instead of letting the market decide, lenders offer certain APR ranges to their customers. They'll often look at things like credit scores instead and offer prime rates to customers with excellent credit and higher rates to customers with subprime credit.

Fixed Rates Pros and Cons

.png)

A fixed rate offers borrowers predictability and stability since the loan’s rate and payments stay the same. They also provide security during economic uncertainty since your rate won’t rise with the market.

However, with a fixed interest rate you may pay more if the market rates go down, and they be a less flexible option since the rate stays the same.

Fixed Rate Loan Examples

There are many kinds of fixed-rate loans, each serving different financial needs and goals. Some common examples include:

- Fixed-rate mortgages: These are home loans in which the interest rate remains constant throughout the loan term, typically 15, 20, or 30 years. This provides stable monthly payments.

- Fixed-rate credit cards: Unlike variable-rate credit cards, these have a consistent interest rate, keeping the cost of borrowing the same over time.

- Payday loans: These are short-term loans that usually come with a fixed interest rate and must be repaid by the borrower's next payday. They are often used for emergency expenses but may come with higher annual percentage rates (APRs).

- Investment bonds: Bonds issued by governments or corporations often come with fixed interest rates, providing predictable returns to investors over a specified period.

- Auto loans: These loans finance the purchase of a vehicle, and fixed interest rates maintain consistent monthly payments throughout the loan term.

- Personal loans: Fixed-rate personal loans are used for various purposes such as debt consolidation, home improvements, or major purchases, offering a steady repayment schedule.

Each fixed-rate loan type offers stability and predictability, making them attractive to borrowers seeking to manage their finances with minimal surprises.

Variable Interest Rates

A variable interest rate is a type of interest rate that changes with the market. This type of rate is linked to a financial index or benchmark that it adjusts to as the market changes. It can also be known as an adjustable rate.

Variable rate payments can vary according to what's happening in the market, meaning you could potentially save money when the market does well. However, that also means you could potentially not save money if the market goes bad.

Variable Rates Pros and Cons

A variable rate offers flexible loan terms, the chance to save on interest as the market goes down, and potentially lower initial costs than a fixed rate.

However, with a variable rate you may pay more as the market goes up, which can lead to higher monthly payments and higher overall borrowing costs. To sum up, variable-rate loans can offer cost savings in favorable interest-rate environments but carry a higher risk of financial volatility.

Variable Rate Loan Examples

There are many examples of variable-rate loans, each serving different financial needs and situations. Some common examples include:

- Variable-rate mortgages (adjustable-rate mortgages or ARMs): These home loans have interest rates that can change periodically based on an index, leading to fluctuating monthly payments. They often start with a lower fixed rate for an initial period before adjusting.

- Variable-rate credit cards: These credit cards have interest rates that can change based on the prime rate or another index, affecting the cost of carrying a balance month to month.

- Variable-rate personal loans: These loans can be used for various purposes, such as debt consolidation, home improvements, or major purchases. Their interest rates can adjust over time, potentially leading to varying monthly payments.

- Investment bonds: Some bonds, particularly certain corporate or municipal bonds, come with variable interest rates that can change based on market conditions or specific benchmarks.

- Home equity lines of credit (HELOCs): These loans allow homeowners to borrow against the equity in their home with interest rates that can change over time, often tied to the prime rate.

- Student loans: Some private student loans offer variable interest rates, which can lead to changing monthly payments over the life of the loan based on market rate fluctuations.

Each variable-rate loan type offers the potential for lower initial costs but comes with the risk of increased payments if interest rates rise, making them suitable for borrowers who can manage the potential financial variability.

Compound Interest Rates

Compound interest means you're earning or paying interest on both the principal and the accumulated interest. Over time, this creates a compounding effect, where interest builds upon itself and grows more rapidly than simple interest.

Compound Interest Pros and Cons

Compound interest is powerful for building wealth, especially when saving or investing over time. However, for borrowers, compound interest can significantly increase the total repayment amount, particularly on credit cards or unpaid balances.

Compound Interest Loan Examples

This type of interest rate is especially useful for investments, so your money can grow! Find savings or investment accounts with compound interest to start growing your investment portfolio today.

- Savings accounts: Interest compounds daily, monthly, or annually, depending on the bank.

- Investment accounts: Long-term investments compound over time to maximize returns.

- Credit cards: Compound interest on unpaid balances increases debt if not paid in full.

- Certain student loans: Some capitalize interest, adding unpaid interest to the loan balance.

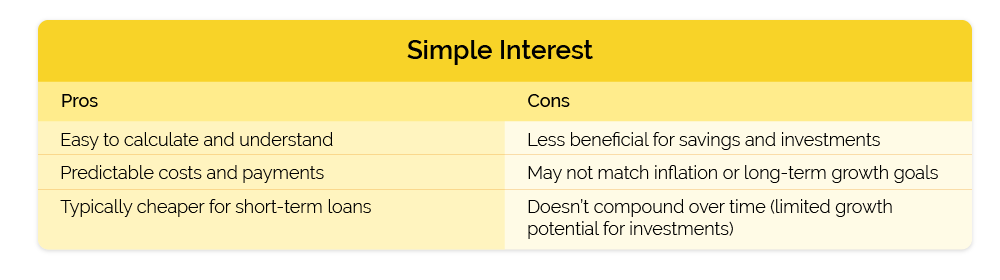

Simple Interest Rates

Simple interest is calculated only on the original amount of the loan or investment. It doesn’t take previously earned interest into account, making it easy to calculate and track.

Simple Interest Pros and Cons

Simple interest works well for short-term loans and those who want straightforward payment terms. It’s also a useful model for borrowers seeking transparency and simplicity in their repayment schedules.

Simple Interest Loan Examples

Simple interest is just that, the simplest type of interest. It’s straightforward and easy to understand and calculate. As an investment you won’t yield as much, but as a loan interest, simple rates are a great way to go.

- Auto loans: Many car loans use simple interest for predictable monthly payments.

- Personal loans: Fixed-term loans that charge interest on the principal only.

- Short-term installment loans: Basic repayment structure with no compounding.

- Savings bonds (some types): Older or government-issued bonds with fixed simple interest returns.

Nominal Interest Rates

The nominal interest rate is the stated rate on a loan or investment, without adjusting for inflation or compounding. It’s the base percentage used to calculate interest payments or earnings.

Nominal Rate Pros and Cons

Nominal interest is a useful way to quote and compare loans, but it doesn’t give a full picture of the loan’s affordability or profitability—especially over time.

Nominal Rate Loan Examples

Check for the nominal rate in your loan or account agreements to get a more detailed view of how interest will be applied to your account.

- Loan advertisements: Lenders often advertise nominal interest rates to attract borrowers.

- Fixed-rate loans: Nominal rates appear in loan disclosures and contracts.

- Bonds and CDs: The nominal rate is printed on the face of the bond or certificate.

- Credit agreements: All loan paperwork includes the nominal rate as a base value.

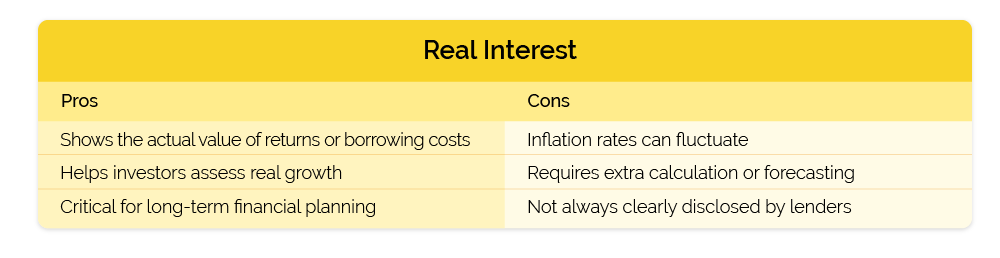

Real Interest Rates

A real interest rate is the nominal rate minus inflation. It represents the true purchasing power gained or lost by a borrower or investor after adjusting for rising prices.

Real Rate Pros and Cons

Real interest rates provide a clearer view of financial outcomes. They help borrowers and investors understand what their money is really worth in today's dollars, especially when inflation is high.

Real Rate Loan Examples

Calculate your real rate to better understand the real worth in today’s dollars of your loan or investment.

- Inflation-linked bonds: Returns are tied to inflation, giving real-rate performance.

- Loan comparisons: Used to evaluate the value of loans across different economic periods.

- Long-term investments: Planning tools for retirement accounts and annuities.

- Adjustable-rate mortgages: Analyzed for real rate performance over time.

Prime Interest Rate

The prime rate is the interest rate banks offer their most creditworthy borrowers. It serves as a benchmark for many other types of consumer and business lending rates.

Prime Rate Pros and Cons

The prime rate serves as a foundational benchmark in the lending world. Many variable-rate loans, including credit cards and HELOCs, are set a certain percentage above the prime rate.

Prime Rate Loan Examples

Look for ways to build credit so you can get the best prime rates with your prime credit score. This will especially help you when applying for the loans you need and qualifying you for the best rates available.

- Home equity lines of credit (HELOCs): Often tied to the prime rate.

- Variable-rate credit cards: APRs fluctuate based on changes in the prime rate.

- Small business loans: May be priced using the prime rate plus a margin.

- Personal credit lines: Typically linked to prime for high-credit borrowers.

Annual Percentage Rate (APR)

The APR is a standardized measure that shows the total annual cost of borrowing, including the interest rate plus any fees or charges associated with the loan.

APR Pros and Cons

APR is one of the most helpful tools when comparing loans side by side. It gives borrowers a better understanding of what they’re really paying over the life of a loan—not just the rate.

APR Loan Examples

Look for the Annual Percentage Rate (APR) so you can easily compare the cost of loans across multiple loan options. This will help you shop for the options with the best rates with a number you can easily compare between lenders.

- Credit cards: APR includes the interest plus annual fees.

- Mortgages: APR reflects interest, points, and closing costs.

- Personal loans: Discloses the total cost including any origination fees.

- Auto loans: Offers a true comparison of dealers and lenders.

The Bottom Line

Understanding the different types of interest rates, whether fixed, variable, simple, compound, or otherwise, can help you make smarter financial decisions when borrowing, saving, or investing.

Each type of rate has its own strengths and considerations, and knowing how they work allows you to better evaluate loans, compare offers, and maximize your financial opportunities.

Whether you're applying for a loan or building long-term savings, having a clear understanding of interest rates puts you in control of your financial future.

This content is for informational purposes only and does not constitute financial or legal advice. Loan products, terms, amounts, rates, fees, and funding times may vary by state and applicant qualifications. All loans are subject to approval and verification under applicable law. Check City is a licensed lender in each state where it operates. Loans are intended for short-term financial needs only. Please borrow responsibly.