What are emergency loans, how do they work, and how do you know if you need one? Learn all of this and more in our article.

Life can be unpredictable with sudden emergency expenses that can come up at any time. Whether you have an unexpected medical bill, a sudden car repair, or damage to your home that urgently needs fixed, an emergency loan could be what you need to get through it.

Let’s explore what emergency loans are, the different types of emergency loans available, how they work, and what you want to consider before applying. This information will help you make an informed decision as you navigate any potential financial crisis.

Get an Emergency Loan at Check City

Check City is here to help when you have sudden, emergency expenses that can’t wait. Our application process is fast and simple, so you can get the funds you need as quickly as possible! Whatever your financial emergency might be, Check City is here to support you through it.

What is an Emergency Loan?

An emergency loan is a type of loan that provides access to immediate financial relief in an emergency situation. It’s a loan designed to offer a financial lifeline when you need it most.

These loans are typically unsecured, meaning they don't require collateral, but some secured loans, like title loans, can be used for emergency financing.

Emergency loans can be used for a variety of unexpected expenses, like medical bills, car repairs, or home repairs, and more. They’re usually a flexible type of loan, like a personal loan, that can be used for a variety of personal reasons.

Types of Emergency Loans

There are several types of emergency loans available to borrowers looking for urgent financial support. Understanding the difference between different emergency loan examples is key to knowing which option is best for you.

Some common examples include personal loans, payday loans, credit card advances, title loans, home equity loans, or general lines of credit.

Personal Loans

Personal loans are a type of flexible unsecured loan that can be used for various personal reasons, including emergency expenses. You can get this type of loan from places like banks, credit unions, and even online lenders.

Payday Loans

Payday loans are a type of short-term loan that can be used when you need fast cash for an emergency. This type of loan is usually used for smaller loan amounts and is generally paid off on the borrower’s next payday. You can find them from online lenders like Check City.

Credit Card Cash Advances

Some credit cards will allow users to withdraw cash from their credit card. But this option is only available with some credit cards and can come with high interest rates and fees.

Title Loans

A title loan is a type of secured loan that uses the value of your car’s title to secure the money you want to borrow. If you need to lean on collateral to get money in an emergency, then this option could work for you.

Home Equity Loans

A home equity loan uses the value of your home or real estate to secure the money you want to borrow. If you need to lean on collateral to get money in an emergency, then you could use your home as collateral to secure the sum you need. These loans can also provide access to larger sums of money but often require a sufficient amount of home equity.

Lines of Credit

A revolving line of credit, like a credit card, can often come in handy in cases of emergency when you don’t have enough saved up and put aside for an emergency situation.

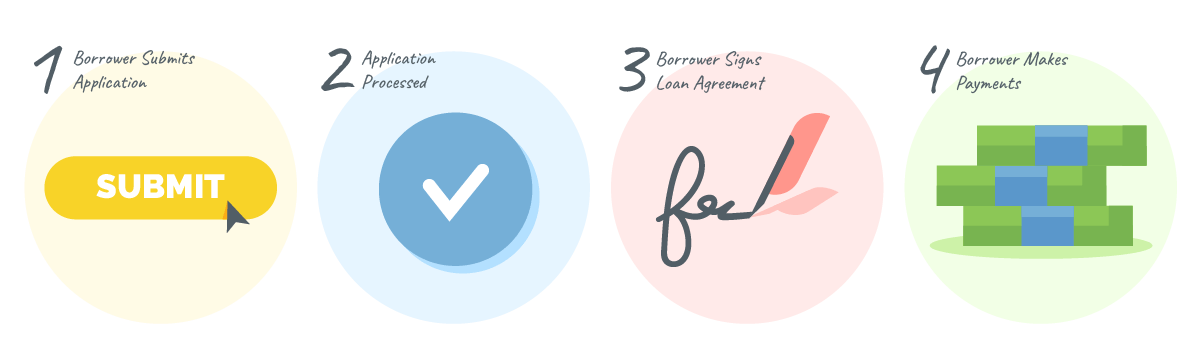

How Emergency Loans Work

Emergency loans work by providing borrowers with a quick and easy way to access funds during a financial crisis. The process typically involves submitting an application, the lender processing the application, signing the loan agreement if you get approved, and making payments until the debt is repaid.

1. Borrower Submits Application

The first step is for the borrower to submit an application for the loan option they’ve selected. Many applications can now be done online, making the process even simpler and faster.

Generally, loan applications ask for basic personal information, like your name, address, and social security number, as well as financial details like your income and employment status.

2. Application Processed

The application is then processed through the underwriting process. In this stage, the lender will verify your information and eligibility. This process may also include a soft or hard credit check to assess your creditworthiness and how well you make debt payments.

3. Borrower Signs Loan Agreement

If your application gets approved, then it’s time to sign the loan agreement and get the emergency money you need disbursed to you. Depending on the lender the application review and disbursement process could happen that same day or in a few business days.

4. Borrower Makes Payments

Now that you have the money you need to tackle your financial emergency, it’s time to enter the repayment cycle. Depending on the lender and the type of loan you selected, you might pay the emergency loan back in one lump sum or several installments. Read your loan agreement carefully before signing to understand your payment schedule.

Emergency Loan Eligibility Requirements

Eligibility requirements for emergency loans can vary depending on the lender and type of loan. Common criteria include requirements like having a good credit score, verifying your income and ability to make payments, having a valid form of identification, and having a bank account.

Credit Score

While some lenders offer emergency loans to borrowers with poor credit, some lenders may require borrowers to have a certain credit score range. Either way, it’s always a good idea to work toward building better credit, since a higher credit score can improve your chances of getting approved for things and get you better loan terms.

Income Verification

Lenders often require proof of a stable income to ensure the borrower can repay the loan. You can verify your income with documents like a recent bank statement or paystub. This helps the lender know you have income sufficient to make repayments.

Identification

If you want to apply for an emergency loan, then you’ll need to have a valid form of identification. This helps the lender verify who you are and prevent fraud. They’ll often require a valid form of government-issued ID like a driver’s license or passport.

Bank Account

Not all lenders will require you to have a bank account, but many lenders require borrowers to have an active bank account for disbursing funds and setting up automatic repayments.

How to Get an Emergency Loan

Step 1: Review Your Finances

Before you get an emergency loan, it’s a good idea to check your personal finances. Check how much money you have in case you already have the money you need in a checking or savings account. You might also already have a line of credit you could use for an emergency.

If you still don’t have the money you need then you’ll want to check your credit score and general financial information like your income and debt-to-income ratio to see where you stand and what options you might qualify to get.

Step 2: Consider Your Options

There are many options available to you in an urgent financial situation. You might have money somewhere in your finances you can pull from, an existing line of credit you could use, or a friend or family member that can help.

If these options aren’t available to you, then there are several types of emergency loans that might best suit your needs.

Step 3: Compare Emergency Loan Options

Compare emergency loan lenders, the types of loans you can use, and the rates available to you. Depending on the lender, you might also be able to prequalify and get an estimate on how much you could borrow.

Step 4: Gather Documents and Apply

Once you’ve picked the lender and type of loan you want to go with, gather the documents you need and fill out your application. You can often submit an application online, over the phone, or in person.

Where can I find an emergency loan?

Emergency loans can be found through various financial institutions like:

- Banks

- Credit Unions

- Online Lenders

- Payday Lenders

- Title Loan Companies

How Fast Can I Get an Emergency Loan?

How fast you can get an emergency loan depends on the lender and the type of loan. Many online lenders can process applications and disburse funds within 24 to 48 hours. Traditional banks and credit unions may take a bit longer, typically a few days to a week. Payday loans and cash advances can often be obtained on the same day. Don’t be afraid to contact lenders to ask about processing times when researching potential lenders.

Reasons to Get an Emergency Loan

There are countless reasons why someone might need to get an emergency loan. Sudden financial situations happen to us every day and sometimes you need a little extra financial help to get you through it.

People might borrow money for emergencies like medical expenses, car repairs, home repairs, unexpected necessary travel, or other unexpected expenses.

- Medical Expenses: Unexpected medical bills can quickly become overwhelming, and an emergency loan can help cover these costs.

- Car Repairs: Cars are essential for commuting to work or running important errands. When car repairs can’t wait, getting an emergency loan can be a practical solution.

- Home Repairs: Sometimes needed home repairs are urgent, like fixing a leaky roof or a broken furnace.

- Unexpected Travel: In case of family emergencies or other urgent travel needs, an emergency loan can cover last-minute travel expenses.

- Other Unexpected Expenses: Any sudden financial obligation that cannot be postponed may warrant an emergency loan.

Tips for How to Start an Emergency Fund

Starting an emergency fund can help you avoid the need for emergency loans in the future. Here are some tips to get started:

- Set a Goal: Determine how much you want to save and set that amount as a goal. Typically you want to have 3 to 6 months’ worth of living expenses set aside for emergencies.

- Budget for Emergencies: Adjust your budget by allocating a portion of your monthly income to go into an emergency fund.

- Automate Savings: Set up monthly automatic transfers to your savings account so you never forget to add to that fund.

- Cut Unnecessary Expenses: Identify and reduce non-essential spending to free up more money for your emergency fund.

- Use Windfalls Wisely: Allocate bonuses, tax refunds, and other unexpected income to your emergency fund to boost your savings quickly.

By understanding emergency loans and taking proactive steps to manage your finances, you can be better prepared for unexpected financial challenges.

Related Products:

This content is for informational purposes only and does not constitute financial or legal advice. Loan products, terms, amounts, rates, fees, and funding times may vary by state and applicant qualifications. All loans are subject to approval and verification under applicable law. Check City is a licensed lender in each state where it operates. Loans are intended for short-term financial needs only. Please borrow responsibly.