Compare the debt avalanche and snowball methods to see which debt repayment strategy best fits your financial goals.

Paying off debt can feel overwhelming, but the right strategy can make a big difference. Two of the most popular debt repayment methods are the debt snowball and debt avalanche.

Each approach offers a different path toward financial freedom, and the one you choose can depend on your mindset, goals, and debt profile. If you're ready to take control of your finances, understanding these strategies is a great place to start. You can also learn more about how to pay off debt faster or explore our budgeting tools and tips.

This article will break down the debt avalanche vs snowball method, comparing how they work, their pros and cons, and how to decide which debt management strategy is best for you. If you're unsure where to start, both options provide a clear step-by-step plan for managing multiple debts, whether you want to save the most money or stay motivated with quick wins.

What is the Debt Avalanche Method?

The debt avalanche method focuses on paying off your debts in order of highest to lowest interest rate. This strategy is all about minimizing how much you pay in interest over time. You continue making minimum payments on all your debts but put any extra money toward the debt with the highest interest rate first. Once that debt is gone, you move on to the debt with the next highest rate.

This method is efficient and can save you money in the long run, especially if your debts have a wide range of interest rates. But because high-interest debts often have large balances, it might take longer to feel a sense of progress.

What is the Debt Snowball Method?

The debt snowball method prioritizes paying off debts from smallest to largest balance, regardless of interest rate. With this approach, you also continue making minimum payments on all your debts, but any extra cash goes toward the debt with the smallest balance first. Once that’s paid off, you “snowball” that freed-up payment into the debt with the next smallest balance.

This strategy offers quick wins and psychological motivation. By seeing debts disappear quickly, you build confidence and momentum, though it may not be the most cost-effective method in the long run since you aren’t considering interest payments.

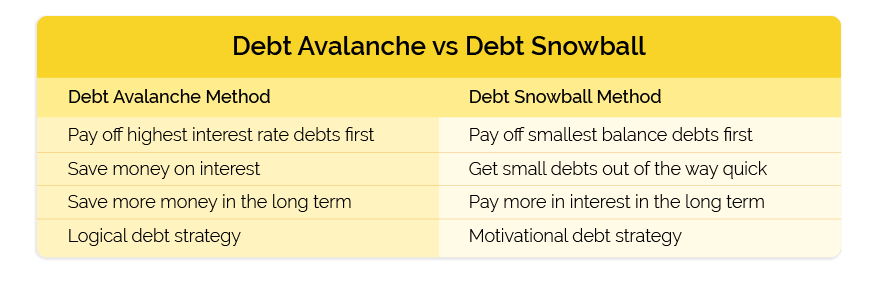

Debt Avalanche vs Debt Snowball

You might wonder, “How does the debt avalanche method compare to the debt snowball method?” Great question! While both methods focus on the same goal of paying down debts, they differ in their strategy for how to do so.

The debt avalanche method pays off debts in order of highest to lowest interest rate, to focus on saving money on interest while you pay off your debts.

The debt snowball method pays off debts in order of lowest to highest amount, to focus on getting smaller balances out of the way first.

As you can see, both strategies have the same goal to pay off debts, but both methods utilize different strategies for how to pay down debts. With the avalanche method you’ll save on interest and with the snowball method you’ll pay off small balances quick.

Debt Avalanche Method Pros

The avalanche method is a smart way to eliminate your debt and interest payments and reduce the overall cost of your debts. With the debt avalanche method, you can:

- Save money on interest

- Pay off your debt faster

- Tackle the debt costing you the most money

Debt Avalanche Method Cons

While the avalanche method of paying off debt is efficient, there are some downsides to consider. This method may feel slow at first and requires strong discipline.

- Requires discipline

- Progress may feel slow

- No immediate wins

Debt Snowball Method Pros

The debt snowball method is another financial approach to tackling your debt. This method is motivating and provides visible progress early on. With this method, you can:

- Quickly knock out the smallest debt first

- See visible progress early on

- Stay motivated with immediate wins

Debt Snowball Method Cons

Despite offering quick wins, the debt snowball has some drawbacks. This strategy feels good early, but may cost you more in the long run.

- Delays your overall progress

- Costs more interest over time

- Not very cost-effective

The Bottom Line

Whether you choose the debt avalanche or snowball method, the most important thing is that you're actively working toward paying off your debts. If you're motivated by numbers, go with the avalanche. If you're motivated by progress, start with the snowball. You can always try out one method to see how it feels and then change strategies if it doesn’t work out for you.

This content is for informational purposes only and does not constitute financial or legal advice. Loan products, terms, amounts, rates, fees, and funding times may vary by state and applicant qualifications. All loans are subject to approval and verification under applicable law. Check City is a licensed lender in each state where it operates. Loans are intended for short-term financial needs only. Please borrow responsibly.