The debt avalanche method prioritizes paying off debts with the highest interest rates first. Find out if it's the right strategy for your financial situation.

Are student loans, credit card bills, and monthly car payments keeping you from growing your savings or booking your dream vacation? What if we told you there was a simple way to knock out your debt so you can save for life’s unexpected moments and celebrate milestones like buying your first home or traveling to your dream destination? You can with the debt avalanche method.

In this article, we’ll share everything you need to know about the debt avalanche method and how it compares to the debt snowball method so you can choose the best approach and become financially free.

What is the Avalanche Method for Paying Off Debt?

The debt avalanche method is a strategy where you list all your debts from the highest interest rate to the lowest. Once you’ve determined the debt with the highest interest, you’ll want to throw as much money as possible to pay off this debt while still making the minimum payment on all your other debts.

After you’ve knocked out the highest interest rate debt, you’ll move on to the next highest interest rate and repeat the process until you’re completely debt-free. Sounds pretty simple, right? We’ll explain more in-depth here soon — don’t worry!

First, let’s discuss how interest rates affect your debt.

How Interest Rates Affect Your Debt

Interest rates play a big role in how much interest you rack up on what you owe before your next payment. For debts with compound interest, like credit cards, interest is added on a daily basis based on the annual percentage rate (APR). That means if the rate is higher, your balance can swell really fast if you’re only making minimum payments.

By focusing on those high-interest debts first using the debt avalanche method, you can cut down on the interest piling up and get rid of your debt more quickly. When interest rates drop, borrowing becomes cheaper, which can help make payments easier and speed up your debt payoff.

Keeping an eye on interest rate changes can really help you tweak your repayment plan to save more money and make progress financially.

How the Debt Avalanche Method Works

With the avalanche debt method, you can reduce the amount you owe and eventually pay off your debt (at least this is the goal, right?). Here’s how:

Step 1: Make a List of Debts and their Respective Interest Rates

Write down a list of your debts (student loans, credit cards, car loans, etc.) and their respective interest rates from highest to lowest. If you can’t remember your interest rate, check your bank statement, review your loan agreement, or contact your bank representative or loan provider for assistance.

Step 2: Find Out Which One Has the Highest Interest Rate

Review your list to determine the debt with the highest interest rate. Once you know, create a budget using paper, an Excel/Google spreadsheet, a budgeting app, or a note on your phone listing your debts and monthly expenses. Your next goal is to calculate how much you can put toward the debt with the highest interest rate.

Step 3: Follow a Budget and Contribute as Much as You Can to Debt Repayment

The trick to sticking with the avalanche method is to follow your budget and contribute as much as possible to paying off the debt with the highest interest rate while making the minimum payment on the others to avoid late fees. Use any extra money from side gigs, work bonuses, or unused funds to knock out as much of your high-interest debt as possible.

One of the simplest ways to stick to your financial goals is to make your budget visible and easy to track. Here are a few ideas you can use to stay focused:

- Take a screenshot of your monthly budget to set as your phone lock screen wallpaper or home screen design.

- Set your Alexa, Siri, or Google Assistant to share a daily/weekly budget reminder.

- Write your budgeting goals on a whiteboard or calendar you see every day.

Step 4: Pay Off the Highest Interest Rate Debt First, Followed by the Next Highest

After you pay off the debt with the highest interest rate, use this extra money from your newly freed payment to put toward the next debt with the highest interest rate — like a financial avalanche — until you’re completely debt-free. Once you’ve tackled the last debt, don’t forget to celebrate and use the extra money to set aside for your savings, investments, or a well-deserved vacation.

Debt Avalanche Method Example

Let’s apply the avalanche method to a real-life scenario.

Imagine you have the following debts with the listed interest rates:

- A credit card balance of $5,000 with a 22.60% interest rate

- A student loan balance of $10,000 at 6.53% interest

- A car loan with a $2,400 balance at 5.49% interest

With the debt avalanche method, you’ll make the minimum payment to your student and car loan while contributing as much money as possible to your credit card balance since that has the highest interest. Once you’ve paid off your credit card, you’ll roll this money over to your student loan and eventually your car loan until you’ve paid all your debts.

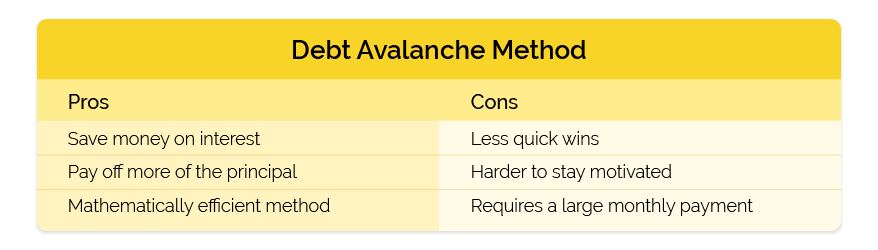

Benefits of the Debt Avalanche Method

The debt avalanche method offers a practical, numbers-driven approach to debt repayment that appeals to people looking to save the most money over time.

By targeting the highest interest rates first, you reduce the overall cost of borrowing and pay off debt more efficiently. While it may not always deliver the fastest wins, this method excels in long-term savings and financial impact.

- Saves Money on Interest. By tackling the most expensive debt first, you lower the total interest paid over time.

- Faster Debt Elimination. Because you're reducing the balance on high-interest debts first, more of your money goes toward paying off principal, not just interest.

- Logical, Math-Driven Approach. This method is the most mathematically logical approach and is ideal if you're motivated by long-term financial savings and efficiency.

Downsides of the Debt Avalanche Method

Although the debt avalanche method is efficient and cost-effective, it isn't perfect for every situation. This strategy relies on patience and discipline, which can be challenging, especially if your highest-interest debt is also your largest debt. Without early wins to keep you emotionally engaged, some people may struggle to stick with this method.

- Less Immediate Motivation. You may not see quick wins if your highest interest debt also has a large balance. This can make it harder to stay motivated early on.

- Requires Budget Discipline. To benefit from this method, you need to consistently make extra payments, which can be difficult if your budget is tight.

Is the Debt Avalanche Method a Good Fit for Me?

If interest rates are slowing your progress, and you’re ready to see more money in your pocket, the debt avalanche method may be the perfect fit for you. With the avalanche method of paying off debt, you can focus on paying off high-interest debt first to save more on interest over time.

Still unsure? Check out the list below to see if the debt avalanche method is the right financial approach for you.

The Debt Avalanche Method Would Be a Good Fit If You . . .

- Are tired of seeing interest overtake your loan or credit card balance.

- Want to break free from an unhealthy relationship with money.

- Enjoy setting and sticking to long-term financial goals.

- Are ready to save money on interest.

- Have a steady income or money from side gigs to make extra payments.

- Want to be financially free.

Final Thoughts

The debt avalanche method is one of the most cost-effective ways to tackle your debt. It prioritizes saving money on interest and long-term goals, helping you pay off your balances faster while saving money too.

Although it may not provide the instant satisfaction of seeing balances disappear quickly, the long-term benefits can be substantial. If you’re ready to take control of your debt and stay disciplined with your finances, the debt avalanche could be the right method for you.

This content is for informational purposes only and does not constitute financial or legal advice. Loan products, terms, amounts, rates, fees, and funding times may vary by state and applicant qualifications. All loans are subject to approval and verification under applicable law. Check City is a licensed lender in each state where it operates. Loans are intended for short-term financial needs only. Please borrow responsibly.