If you find yourself needing help getting approved for a loan, then you might need to know the definition of cosigning and how this practice can help you get approved for the money you need.

There are many instances where a prospective borrower might need some extra help getting approved for the loan they need.

Loan underwriting can be an involved process with many factors that go into determining whether you can get approved for a loan or not. Your credit score, how much debt you already have, and how much you make can all go into the ultimate decision to approve your loan or not.

When one or more of these items isn't enough to get you the loan funding you need, it might be time to bring in a cosigner.

The Definition of a Cosigner

So, what is a cosigner? A cosigner is someone who also signs an agreement. This term can be used for signing many kinds of contracts, but it is seen most often in finance as a term for the secondary signer for a loan agreement.

A cosigner can be defined as a joint signer or the secondary signer of an agreement of some kind. But what does it mean to be a cosigner?

Cosigning is when a cosigner signs an agreement along with the primary signer. This helps establish more security for the lender, allowing it to be easier for the borrower to get approved for the money they need.

By cosigning, this person now promises to take responsibility for the terms of the agreement along with the primary signer. This means that if the primary signer fails to pay back the loan, it will become the cosigner's responsibility.

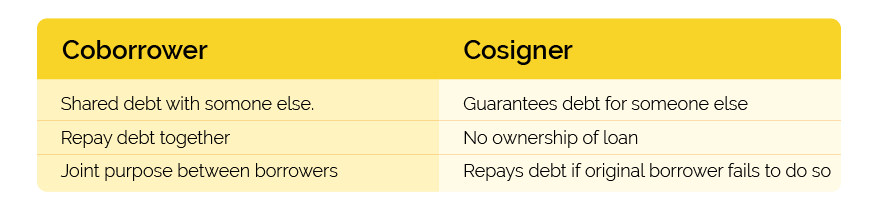

Cosigner vs Coborrower

What is the difference between a cosigner vs coborrower? The biggest difference between these 2 terms is how the co-person is involved in the loan.

A cosigner doesn't take as much responsibility for the loan as a coborrower. A cosigner doesn't own any part of the loan. They just will be responsible for paying back the loan if the original borrower fails to pay back the loan.

A cosigner is most often used in a scenario where the applicant has a low credit score and asks a family member with better credit to cosign with them.

A coborrower can also be referred to as a co-applicant. They take on more responsibility for the loan than a cosigner. A coborrower has partial ownership over the loan. They are expected to make payments toward the loan, and not only if the main borrower fails to pay.

A coborrower is most often used in a business scenario where to business partners want to take out a business loan together.

What Does it Mean to Cosign?

So, how does cosigning work? The very first thing that needs to happen is figuring out whether you need a cosigner or not. Normally, your lender might let you know you can't approve for a loan on your own. Then you can ask your lender if they allow cosigners. So, if you got preapproved for a loan, odds are you won't need a cosigner.

Once you know whether you need one, and whether you can use one, you'll need to find and ask someone to sign jointly with you on this loan. Many people end up asking people they are close to, like family members.

Whoever you ask to sign along with you, they have to be willing to legally take on the responsibility of repaying the loan if you fail to do so.

Cosigning does not mean that the joint signer has any ownership over the loan funding. The primary signer is still the one receiving and paying for the loan. This action is jut an added security measure that borrowers can use in the application process to get approved.

What Kind of Loans Can Get Cosigned?

Most of the loans that involve cosigning will be loans where there is a primary borrower, and the secondary signer is just helping the primary borrower get approved for the money they need.

Some of the most common kinds of loans that can get cosigned include personal loans, installment loans, business loans, and mortgage loans.

Essentially, the kinds of loan that might need this feature are loan types that are larger and include more requirements for their borrowers to meet. By that logic, smaller, short-term loans can be another great option for someone who needs money but can't get a cosigner for a larger loan.

In Conclusion,

Loans come with many requirements. And the bigger the loans the more requirements that loan application will include. But loans can help us afford things big and small, like the money we need to start a business, pay bills or rent, get a car, or buy a home.

This content is for informational purposes only and does not constitute financial or legal advice. Loan products, terms, amounts, rates, fees, and funding times may vary by state and applicant qualifications. All loans are subject to approval and verification under applicable law. Check City is a licensed lender in each state where it operates. Loans are intended for short-term financial needs only. Please borrow responsibly.