Discover the difference between short-term and long-term loans and how they affect your credit.

TLDR: Short-term loans are best for quick access to small amounts of money and are repaid within a year. Long-term payments are ideal for large purchases and can be spread out over several years into monthly installments. Both loans are beneficial depending on your financial situation.

Taking out a loan can be a helpful way to pay bills when money is tight or you need to make a big purchase. However, not all loans function the same way. Some are short-term, meant to be paid back quickly, while others are long-term, giving you more time to repay but often at a larger cost.

In this article, we’ll break down the differences between a short-term and long-term loan to help you determine which one is best for your financial situation.

What is a Loan Term?

A loan term is the length of time over which you agree to repay a loan. Short-term loans are typically less than 1 year in duration, with higher monthly payments but lower interest rates. Long-term loans span from 3 to 30 years, offering lower monthly payments but higher overall interest rates.

Regardless of the loan type, your loan amount plays a role in determining your monthly payment and the total interest you’ll pay.

What are Short-Term Loans and How Do They Work?

Short-term loans are small amounts of borrowed money to be repaid within 1 year or less. Because they have a shorter payment term, these loans often come with higher interest rates than long-term loans.

A short-term loan typically ranges from $100 to $5,000 and requires repayment in either a single lump sum or through small installments over the loan term. For example, if you have a short-term loan of $500 with a 3-month loan period, you must repay the $500 and any accrued interest within this timeframe.

The most common types of short-term loans are:

- Payday Loans: Small loans used to cover expenses until your next paycheck.

- Title Loans: Loans that use your vehicle’s title as collateral and allow you to borrow money based on your car’s value.

- Personal Loans: Flexible short-term personal loans used to cover emergency expenses or small purchases.

Short-term loans are helpful in times of need to keep you covered between paychecks.

Advantages and Disadvantages of Short-Term Loans

While short-term loans can provide quick financial relief, they also come with a few trade-offs. Let’s take a look at the advantages and disadvantages of short-term loans to see if this loan is right for you.

What are Long-Term Loans and How Do They Work?

Long-term loans let you borrow large amounts of money, but they take longer than one year to repay. Because they have a longer term, these loans usually come with a lower monthly payment and a higher interest rate.

Most long-term loans typically range from $5,000 to $100,000, depending on the purpose of the loan. Once you’ve borrowed the money, you’re required to pay monthly installments over the life of the loan. For example, if you have a long-term loan of $20,000 with a 5-year repayment term, you would repay $20,000 plus interest in monthly installments spread over 60 months.

The most common types of long-term loans are:

- Mortgage loans to buy a home

- Auto loans to purchase a new car

- Student loans to pay for tuition and college expenses

- Business loans to start or grow a business

Long-term loans are a great option if you need to borrow a large amount of money and have the flexibility within your budget to repay it over an extended period.

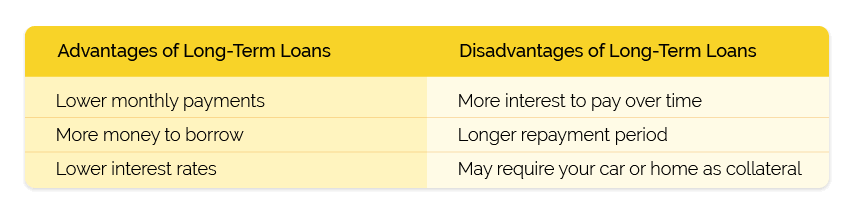

Advantages & Disadvantages of Long-Term Loans

While long-term loans offer the convenience of spreading payments out over time, they also have their disadvantages. Here are a few benefits and drawbacks of long-term loans to consider:

How Do Loan Terms Affect the Cost of Credit?

The length of your loan can significantly impact the total amount you pay. Short-term loans allow you to clear your balance quickly and pay less interest overall. Long-term loans tend to have lower interest rates upfront; however, the total interest can add up over time.

While longer loans are more manageable, they’re often secured, meaning you might need to pledge assets like your home or car as collateral if you can’t keep up with payments.

Short-Term vs Long-Term Loans: Which is Better?

The right choice between a short-term and long-term loan largely depends on what you need to borrow money for and the amount you require. Here’s a quick guide to help you decide which option might be best for you.

When Should You Choose a Short-Term Loan?

A short-term loan might be the best option if you’re looking for:

- Fast access to cash: Cover unexpected emergencies or urgent expenses quickly.

- Smaller loan amounts: Typically ideal for loans under $5,000.

- Quick repayment: Pay back the loan in a few months rather than stretching payments out over several years.

When Should You Choose a Long-Term Loan?

A long-term loan is often the better choice if you need:

- Large purchases: Finance significant expenses, such as a car, home, or business investment.

- Manageable monthly payments: Spread your payments out to make them easier to manage with your budget.

- Long-term stability: Consistent, predictable payments help you plan out your financial goals, especially if you’re looking to get out of debt.

How Check City Can Help You Choose the Right Loan

At Check City, we offer a range of loan options, from short-term to long-term, tailored to meet various needs, including emergency expenses and large purchases. Use our loan comparison tool to evaluate your options and contact us today if you have any questions.

The Bottom Line

Both short-term and long-term loans offer advantages and disadvantages. Short-term loans are perfect for temporary coverage, while long-term loans are best for larger purchases. Either way, it’s important to understand your financial needs and compare loan options to determine the right fit for you.

Key Takeaways

- Short-term loans are best for emergencies, small loan amounts, and quick repayment.

- Long-term loans are best for large purchases and manageable monthly payments.

- Always consider interest rates, repayment terms, and whether collateral is required before taking out a loan.

This content is for informational purposes only and does not constitute financial or legal advice. Loan products, terms, amounts, rates, fees, and funding times may vary by state and applicant qualifications. All loans are subject to approval and verification under applicable law. Check City is a licensed lender in each state where it operates. Loans are intended for short-term financial needs only. Please borrow responsibly.