There are a number of mortgage loan types to consider when buying your home. Understand the pros and cons of each home loan option to make the best decision for you and your house.

Whether you are looking for a home or just browsing the market, it can be helpful to understand how mortgage loan types work and what the different mortgage loan types are. Mortgage loans come in many shapes, sizes, and types.

2 Mortgage Rate Types

One of the first characteristics of a mortgage loan type is the type of rate attached to the loan. Mortgage loans have 2 types of rates. Some loans can even include both of these mortgage rate types. For example, a loan could start off with a fixed rate for a certain amount of time, but then switch to an adjusted rate mortgage later.

Fixed Rate Mortgage

A fixed rate mortgage has an interest rate that stays the same throughout the life of the loan. This mortgage loan type also keeps your monthly mortgage payments the same throughout the life of the loan.

Adjusted Rate Mortgage

An adjusted rate mortgage has an interest rate that changes throughout the life of the loan. The interest rate of an adjusted rate mortgage, or ARM, can fluctuate both up and down based on the current mortgage interest rate market.

8 Mortgage Loan Types

There are many types of loans for homes. Different mortgage loan types come with different loan rates and loan terms, but there are other important characteristics to consider as well.

Conventional Mortgage

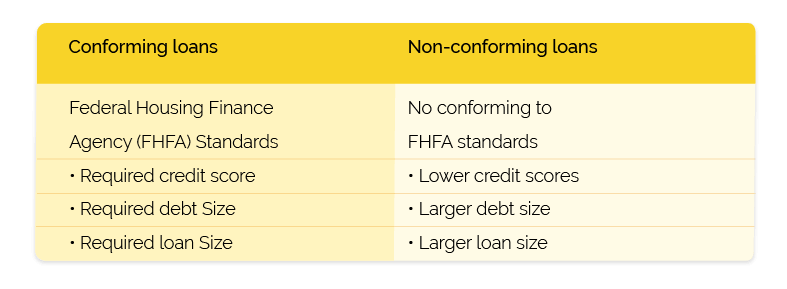

A conventional mortgage loan is a mortgage loan type for homes that is not backed by the federal government. Conventional mortgages also come in 2 types: conforming loans and nonconforming loans.

Conforming loans are the type of conventional loan that conforms to Federal Housing Finance Agency (FHFA) standards. These standards outline items like required credit scores, debt size, and loan size.

Nonconforming loans are the type of conventional loan that do not conform to FHFA standards. These loans can end up allowing lower credit scores and larger debt or loan sizes than FHFA standards allow.

Jumbo Loan

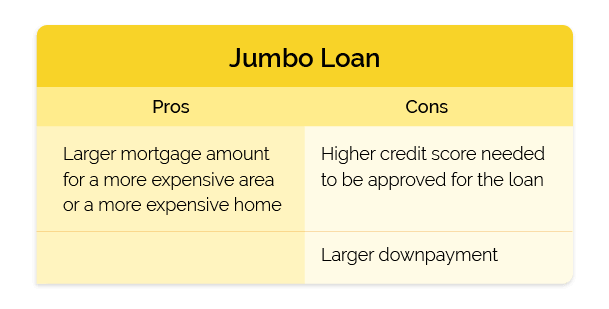

A jumbo loan is a mortgage loan type that does not follow FHFA standards in that their loan amount limits are much higher than FHFA guidelines dictate. These loans can be helpful for homes or real estate areas that are more expensive than the average.

The jumbo loan pros mean that you can get a larger mortgage amount for a more expensive area or a more expensive home. But the jumbo loan cons mean that you may need to pay a larger down payment and have a high credit score in order to get approved for a jumbo loan.

Government-Insured Loan

If your mortgage lender offers government-insured loans, then they probably follow the guidelines set by government organizations like the Federal Housing Administration (FHA), the US Department of Agriculture (USDA), and the US Department of Veterans Affairs (VA). Sometimes loans that follow these government agencies for mortgages are called FHA loans, USDA loans, or VA loans.

These 3 different agencies that help provide government-insured loans, help make home ownership possible for certain borrowers.

Interest Only Mortgage

An interest only mortgage loan type is a home loan that lets borrowers pay interest first. This means that for the first few years, your monthly mortgage payments will be going toward the interest on your loan. Then, later, your monthly mortgage payments will include the principal loan amount.

An interest only mortgage can help people who want to buy a home get smaller initial mortgage payments. This can be a great option for home buyers who want to get into a house but need smaller monthly housing payments to start off with.

Package Loan Mortgage

A package loan mortgage is a type of real estate loan that is secured by real estate and includes the other personal property and furniture found on the property.

This type of home loan may appear more often in the purchase of real estate like fully furnished condominiums or apartments. A package mortgage loan type could also include real estate loans for restaurants or other types of commercial property that might include things like equipment on the premises.

Construction Loan Mortgage

A construction loan mortgage is a type of mortgage loan you’ll need if you’re building your home. You can get a separate construction loan for the construction of your home and for your home mortgage. You can also get one construction loan that covers the home building and the mortgage. When you combine these home loans together it can be called a construction-to-permanent loan.

Piggyback Loan Mortgage

A piggyback loan is a type of home loan that is split into 2 loans and a down payment. The first piggyback loan is for 80% of the home and the second piggyback loan is for 10% of the home. Then, the third part of the piggyback loan is the 10% down payment. Sometimes this mortgage type can be referred to as an 80/10/10 loan, because it involves an 80% loan, a 10% loan, and a 10% down payment.

This type of loan helps home buyers avoid private mortgage insurance (PMI). Avoiding PMI payments can be nice, but using a piggyback loan will mean you have 2 loans to pay off, 2 loans accruing interest, and 2 sets of closing costs to deal with too.

Balloon Mortgage Loan

A balloon mortgage loan is a type of mortgage loan that starts off with regularly sized monthly payments, but at the end of the loan’s life, there is a large payment to be made. This loan can help home buyers have regular payments for now, but will require a large payment in the future, which can be difficult if your finances are not ready for a large balloon mortgage payment in the future.

In Conclusion,

There is a lot to know as a home buyer, like how real estate works, closing costs, and more. But if you want to buy a home then you first need to do your research on things like mortgage loans. Understanding different types of mortgage loans and how they work can help you make the right choice when shopping for a home loan.

This content is for informational purposes only and does not constitute financial or legal advice. Loan products, terms, amounts, rates, fees, and funding times may vary by state and applicant qualifications. All loans are subject to approval and verification under applicable law. Check City is a licensed lender in each state where it operates. Loans are intended for short-term financial needs only. Please borrow responsibly.