Learn more about what tax liability is, what it means for you and your tax responsibilities, and how to calculate this number when you're filing.

All individuals, organizations, and businesses have a tax liability to the federal, state, and local governments they live in. If you are a business, then you may be familiar with tax liability as an item on your business's accounting records. If you are an individual taxpayer, then you may have heard this tax term before, but you might still be confused about what it means or how it applies to you.

In this article we'll go over not only what tax liability means, but how it applies to both individuals and businesses so you can file your taxes correctly and avoid unnecessary audits.

What is Tax Liability?

Tax liability is a tax term used by the Internal Revenue Service (IRS) and tax professionals when referring to someone's tax responsibility. Someone's tax liability is the total amount of taxes they are responsible for, or rather, the total amount of taxes they owe. Usually, this tax liability is calculated per year. When we file taxes at the beginning of each year from January to April, we are calculating our tax liability for the previous year. You may have already paid what you owe in taxes with payroll taxes, or you might get a tax bill from the IRS with the amount you still owe.

Both businesses and individuals owe taxes to their local, state, and federal government. When you're filing your 1040 tax forms, you'll calculate your tax liability, or how much you owe in taxes, to your local, state, and federal government.

Business Tax Liabilities

Taxes work very differently for businesses than they do for individuals. They have their own tax laws and requirements to consider. A business's earned income is also very different from an individual's earned income. But one thing business tax liabilities have in common with individual tax liabilities is that they are both due in the next year.

Business tax liabilities are considered short-term liabilities and are kept in a special section on their balance sheet. This is because they are payments that will need to be made in the next year, rather than at a later date. Part of a business accountant's job will be to keep the business's financial records, file their taxes, and calculate the taxes they need to pay to the local, state, and federal government.

Individual Tax Liabilities

If you are an individual taxpayer than you are probably more familiar with how taxes work for you. Many individuals will pay their taxes throughout the year in sales tax and payroll taxes, rather than paying a tax bill later on like business's often do. These tax payments are also called withholdings and can be found on the W4 form you filled out when starting your current job.

What is Liable to Tax?

What individuals and businesses need to pay in taxes grows with each taxable event. These events are things that are subject to taxation. The most common instance of tax liability is when an individual or business earns income. We call this earned income tax and individuals and businesses owe earned income tax every year.

But there are other tax liable situations like when you buy or sell something or when a business issues payroll to their employees. You might see sales tax when you go to buy something and have to pay a little extra then the price tag amount. You might see payroll tax when you get a paycheck and see that a certain amount of your income went to pay things like Medicare and Social Security.

Another instance where you might run into tax liability is when you own property. If you own land, a home, or other forms of personal property, then you may have to pay property taxes on those items.

These are the main instances where you will accumulate tax liability. When you buy or sell something, earn money, or own certain kinds of property.

What is Federal Income Tax Liability?

Federal income tax liability is specifically how much you owe in taxes to the federal government. Each year taxpayers earn income and owe taxes on that earned income. A percentage of your income tax goes toward the federal government.

How much you make annually will put you in a federal tax bracket. Your tax bracket will then give you a tax rate percentage for how much you'll owe in taxes based on how much you made in a year. If your annual earned income is below a certain amount, then you'll actually be exempt from owing federal income tax.

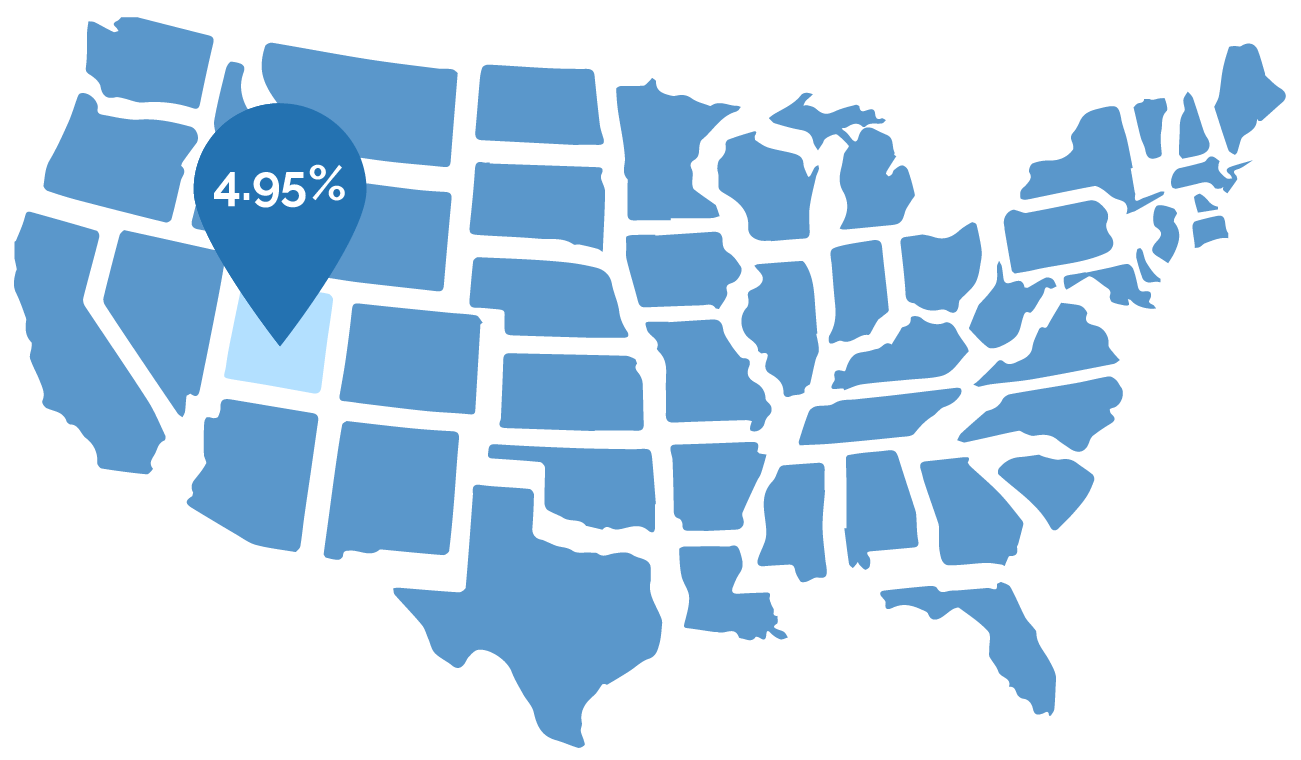

What is State Income Tax Liability?

State income tax liability is specifically how much you owe in taxes to the state government. Each year taxpayers earn income and depending on your state, you may owe a state income tax on what you earned.

Research your state's income tax laws and income tax rate. These details will be different for every state. For example, Utah's income tax rate is 4.95%, so taxpayers in Utah will owe 4.95% of their earned income to the state government in state income tax.

How to Calculate Tax Liability

To calculate your tax liability, you'll need to become familiar with terms like gross income and adjusted gross income. In order to calculate how much you owe in taxes, you first need to figure out your gross income amount.

Once you have your gross income, you can calculate your adjusted gross income or AGI. Once you have your AGI, you'll know your taxable income amount. Once you know how much of your income is taxable, you can then calculate how much you owe in taxes based on your tax bracket and tax rates.

Tax Liability Calculations:

- Calculate gross income

- Calculate adjusted gross income

- Calculate tax liability with the tax rates applied to your taxable income

Is Taxes Payable a Current Liability?

Yes. Tax payable is a tax term used mostly by companies. It refers to a type of account in a business's balance sheet or accounting records. This account is found in the current liabilities section of this balance sheet. Tax payables are an item in the current liabilities section because they are taxes that the company owes and must pay within the next year.

Essentially, tax payables and current liabilities are a way for companies to reference the taxes they owe the soonest. Then, deferred taxes will not be in this current liabilities section since their payments aren't due until a later date.

How to Reduce Tax Liability

The main way you can reduce your tax liability is to reduce your taxable income and assets. Taxes are mainly posed on income and assets, like personal property, bonds, or investments.

You can reduce your taxable income by using tax deductions and credits available to you. There are tax credits for parents and homeowners available to help lower your overall tax obligation. You can reduce your taxable assets by lowering the amount of taxable assets you have. For instance, renting instead of owning a home will help you avoid property taxes.

In Conclusion,

Everyone has tax liabilities, including companies. So it's important to make sure you understand all the taxes you are responsible for, especially if you have a small business or are self-employed at all. It's also important to keep the things you own in good shape. For example, taking care of your car by paying attention to the mileage.

This content is for informational purposes only and does not constitute financial or legal advice. Loan products, terms, amounts, rates, fees, and funding times may vary by state and applicant qualifications. All loans are subject to approval and verification under applicable law. Check City is a licensed lender in each state where it operates. Loans are intended for short-term financial needs only. Please borrow responsibly.