FSA and HSA accounts are 2 types of healthcare savings accounts. Learn more about these key differences so you can decide on which type of healthcare savings account is best for you.

Did you know that you could open a savings account specifically for healthcare savings? These types of accounts are called FSA and HSA accounts.

These accounts are similar in that they both can help people safely put away money and build savings for medical expenses. FSA and HSA accounts can even help you save more on your taxes each year. Check City's professional tax services can also help you get the most out of your tax refund.

Even though they are similar in many ways, there are a lot of important differences to know when researching FSA vs HSA accounts, as well.

They work differently with contributions, who manages them, who qualifies for them, and how they are treated for tax returns as well. Take the knowledge you gain about FSA vs HSA accounts to make the best choice for you and your finances.

What is FSA and HSA?

Before you can understand the difference between FSA vs HSA accounts, you'll need to know more about each one.

So what does FSA stand for? What does HSA stand for? The terms FSA and HSA are acronyms for Flexible Spending Account (FSA) and Health Savings Account (HSA).

Sometimes the IRS will also refer to a Flexible Spending Account as a Flexible Spending Arrangement.

Both FSA and HSA accounts are savings accounts. But they aren't just any type of savings account. These accounts have a specific purpose—to save money specifically for medical costs. These accounts allow people to set aside money into a safe savings account specifically for paying medical expenses.

The medical expenses that these accounts can be used for include:

- Medical care

- Prescription drugs

- Dental care

- Vision care

- Over-the-counter medications

What is an FSA Account?

A Flexible Spending Account (FSA) is a type of savings account that allows employees to save pre-tax dollars to help pay for eligible medical, dental, and vision expenses.

It's only available to an employee whose employer offers a benefits package that includes an FSA. This is the only requirement for getting an FSA account.

These accounts are owned by your employer, rather than the individual, and cannot be carried over as you change employers.

Withdraws from an FSA account are dependent on how your employer set up the account. For some FSAs, the funds available to you will expire after a certain period of time. Sometimes a certain amount will be allowed to roll over into the next year, but not always.

Because the owner of the account is the employer, the employee may have to submit their medical expenses to their work in order to get reimbursed from this benefits package.

What is an HSA Account?

A Health Savings Account (HSA) is a type of savings account that helps people with a high-deductible health plan (HDHP) save tax-free money to pay for eligible medical expenses.

There are a few other requirements to know about as well besides needing to be covered by a High-Deductible Health Plan. For example, to qualify for an HSA account you cannot be claimed as a dependent on anyone's tax return and you cannot be enrolled in Medicare.

HSA accounts can even be used as a retirement savings account specifically for saving up for medical expenses during retirement.

What are the Differences Between HSA and FSA?

Although FSA and HSA accounts are a similar type of savings account, there are also many differences between FSA vs HSA accounts. If your employer offers an FSA and you also have an HDHP, then you might have to choose between an FSA vs HSA option.

Some of the primary differences between FSA vs HSA accounts include who these types of accounts are available to, who owns the account, and how contributions work.

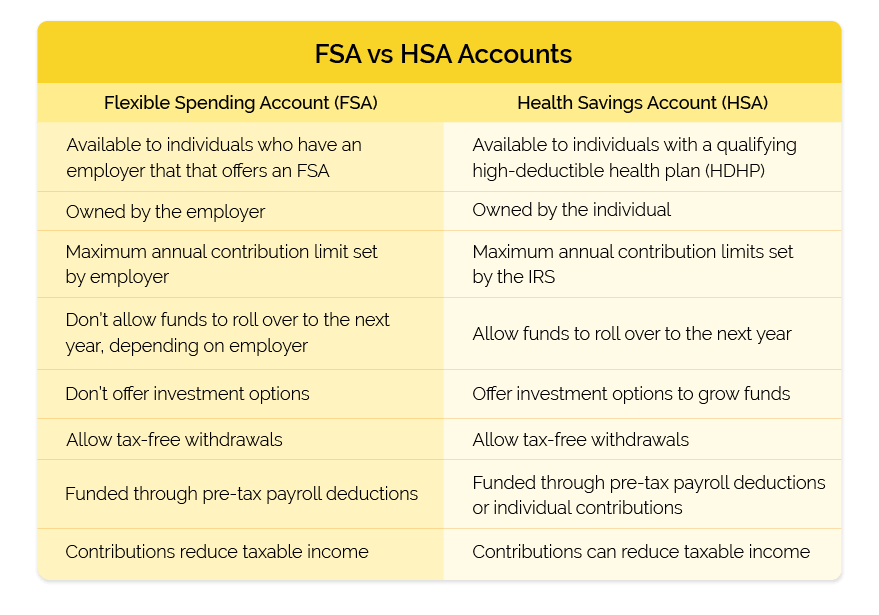

For example, an FSA is available to available to individuals who have an employer that offers it, and an HSA is available to individuals with a qualifying high-deductible health plan (HDHP).

An FSA is owned by the employer, but an HSA is owned by the individual.

An FSA has a maximum annual contribution limit set by the employer, while an HSA has a maximum annual contribution limit set by the IRS.

An FSA does not allow funds to roll over to the next year if they aren't used (this can depend on the employer who may offer a grace period), but an HSA does allow unused funds to roll over to the next year.

An FSA does not offer investment options, while an HSA does offer investment options to grow funds.

Both accounts allow tax-free withdrawals, and can be funded through pre-tax payroll deductions, meaning contributions to both accounts can potentially reduce taxable income. But HSA accounts also allow individual contributions from post-tax dollars.

Can I have both an FSA and HSA account?

It is not likely that you would have both an FSA and HSA account. But it is possible under very specific circumstances. If you qualify for an HSA and you have an employer that offers an FSA that does not have a "limited-purpose," then it's possible you could set up both of these accounts.

If you qualify for an HSA and your employer offers an FSA, but it does have a "limited-purpose," then you won't be able to open both of these accounts at the same time. Instead, you'll have to choose one or the other.

How are FSA and HSA accounts tax advantaged?

One of the perks of using one of these special savings accounts is that they have special tax savings available.

FSA contributions come from pre-tax money taken out of your paychecks before taxes. This means that FSA contributions do not count as a tax deduction toward income tax. But the contribution amounts to an FSA do reduce your overall taxable income.

HSA contributions are tax free going in and out of the account, so long as these contributions are used for qualifying medical expenses and not something else. These contributions are not subject to income tax. Interest earnings in this account are also not subject to income tax.

How Does an FSA Work?

An FSA is an employer-based savings account set up to pay for qualified medical expenses. If the employee ops in for this account, then they will be given a debit card connected to the FSA funds available to them per plan year. This card can then be used for qualifying medical expenses. Employees might also not get a debit card connected to their account, and instead they might have to submit receipts for the medical expenses they would like to get reimbursed.

The money on an FSA card can sometimes roll over between plan years, but can also sometimes expire after a certain amount of time. Some FSA plans will include a grace period, like an extra 2 months, to give employees an extra chance to use those funds.

The funds in this account are usually taken out of each paycheck, but the full account amounts are usually available to spend at the beginning of the plan year.

Many of the aspects for how this plan will work are chosen by the employee at open enrollment. During open enrollment you can decide things like the contribution amount you want taken from your paycheck.

How Does an HSA Work?

An HSA is an employee-based savings account set up to pay for qualified medical expenses. If a person qualifies for an HSA by having an HDHP, then they can set up this type of savings account. They will normally also be given a debit card connected to the HSA account. This debit card can then be used for qualifying medical expenses.

The money on an HSA card is put there by the account holder rather than taken from the employee's paychecks. Though there are some employers that offer to contribute paycheck earnings to employee HSAs if they wish to set that up.

Many of the aspects of an HSA account depend on which provider you decide to go with. There are several banks and other financial institutions that offer HSA accounts to their qualifying customers.

This content is for informational purposes only and does not constitute financial or legal advice. Loan products, terms, amounts, rates, fees, and funding times may vary by state and applicant qualifications. All loans are subject to approval and verification under applicable law. Check City is a licensed lender in each state where it operates. Loans are intended for short-term financial needs only. Please borrow responsibly.