Learn what is adjusted gross income, how it relates to gross income, and when you might need to calculate this number for financing and taxes.

Income is one of the founding pillars of finance and financial planning. But did you know that there are different kinds of income, and different ways of calculating that income? Your earned income can be calculated as either gross income or net income. There are also different types of gross and net income, like adjusted gross income (AGI).

Having a thorough understanding of income and how it is calculated is important not only for your personal budgeting, but for investments, financial planning for now and the future, and for filing tax returns. This will help you become a better financial planner in your personal and professional life, and it will help you file accurate tax returns.

AGI vs Gross Income

Adjusted Gross Income can also be referred to as AGI in the finance world. Abbreviations like this make life just a little bit easier when talking finance like a pro.

But before we get into AGI and all it entails, we'll need to take a step back and talk about gross income. To understand what adjusted gross income is, you first need to understand what gross income is, because AGI is a number that comes from gross income.

Put as simply as possible, gross income is your total income before taxes. This is like the base amount of money you earn from all sources of income. It is also the total amount of money you earn before any taxes or deductions have been taken out of it. So, income tax, payroll tax, health insurance payments, and more, haven't taken their shares yet.

Adjusted Gross Income Definition

Adjusted gross income (AGI) is your total income, adjusted. But adjusted how? It is your total income with some basic taxes taken out. It should not be confused with net income, which is your total income after all your taxes. Adjusted gross income does not apply all taxes like net income does.

Instead, AGI only considers a few items called "adjustments." These adjustments are the types of taxes, credits, expenses, or deductions that are included in the AGI calculation. The following is a list of adjustment examples that could be included in your AGI calculation:

Example Adjustments:

- Business expenses

- Student loan interest payments

- Alimony payments

- Early withdrawal penalties on savings

- Educator expenses

- Employee business expenses for armed forces reservists

- Qualifying performing artists

- Some state or local government officials

- Employees with impairment-related work expenses

- Health Savings Account (HSA) deductions

- Moving expenses for members of the armed forces

- Self-employed Simplified Employee Pension (SEP)

- Savings Incentive Match Plan for Employees of Small Employers (SIMPLE)

- Other qualifying retirement plans

- Self-employed health insurance deduction

- Qualifying self-employment tax

- Other qualifying expenses

When to Use AGI

Adjusted gross income can be used for many reasons, but the two main reasons that an average person might want to know how to calculate AGI, is when they are creating a monthly budget, or when they are filing taxes.

Use AGI to File Taxes

AGI is a number that is primarily used by tax filers and the IRS when determining an individual’s tax liability. Tax liability is the IRS’s term for someone’s tax responsibility, or how much someone owes in taxes each year. How much you owe in taxes greatly depends on how much money you make in a year. How much you make will determine your tax bracket, which will determine the percentage of your yearly income that is subject to income tax.

A taxpayer's AGI is the number the IRS uses to say how much you make in a year and thus, which tax bracket or income bracket you belong to. They could instead use gross income as their starting point, but these adjustments help take into consideration things like business or student expenses that income was needed for. Expenses like that can come with tax deductions, so including them to adjust how much you make will also adjust how much you owe in taxes, helping you out in the long run.

Use AGI to Budget

You'll mostly want to use AGI when filing taxes, but there are instances in personal financial planning where knowing how to calculate this number could be very useful. When creating a monthly budget and monthly spending plan, it helps to know how much money your bank account will actually see each month. This will give you a more realistic idea of how much you have to spend. Once you have this number you can more accurately plan for your daily and monthly expenses and bills.

How is Adjusted Gross Income Calculated?

As we’ve said before, AGI isn’t the same as net income, it does not consider all taxes on gross income, only some of them. The taxes that AGI includes in its calculations are payments and expenses that are tax deductible, or don’t count toward your taxable income.

If you use a tax preparation service or tax filing software, this software will take your income numbers from your W2 and 1099 forms and calculate the AGI for you. But if you are doing things old school and filling out your tax return 1040 form yourself, then here is how you’ll calculate AGI:

- Add together all sources of income for the year.

- Subtract all the adjustments that apply to you from the adjustment examples listed above.

- The number you are left with is your estimated AGI for that year.

Adjusted Gross Income (AGI) vs. Modified Adjusted Gross Income (MAGI)

The IRS may also use another type of adjusted gross income known as Modified AGI or MAGI. This income calculation is used specifically for retirement accounts and other special programs.

Remember how AGI is your gross income number, but adjusted? MAGI is your AGI number, but modified once more. To calculate your MAGI, you or your tax filing service will start with your AGI number and then add back some items that were taken out when calculating AGI.

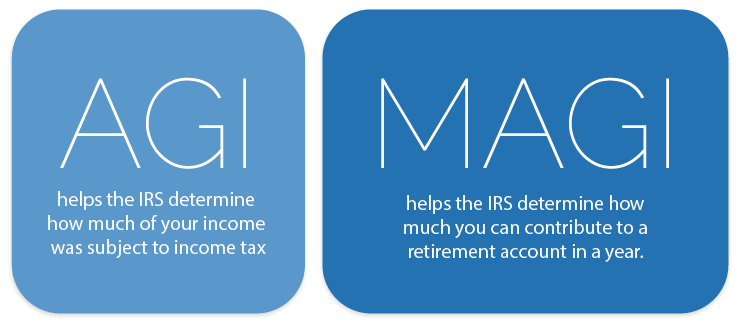

But what is MAGI used for? AGI helps the IRS determine how much of your income was subject to income tax, while MAGI helps the IRS determine how much you can contribute to a retirement account in a year. Some retirement accounts, like a Roth IRA, have contribution limits based on how much money you make.

MAGI is also used when applying for Marketplace Health Insurance. This type of insurance falls under the Affordable Care Act (ACA) and has its own income requirements. MAGI is the income calculation used to find an applicants annual income.

Adjusted Gross Income on W2 Forms

Adjusted gross income is mostly used by the IRS and in taxes. This number goes on your tax return, the document used to report and submit your filed taxes each year. Your tax return form is also known as the 1040 tax form.

You can find the spots where AGI goes on line 37 of the standard 1040 form, line 21 or the 1040A, and line 4 on the 1040EZ. Once this number is calculated and submitted on your 1040 Tax Return form, keep the number handy for next year. A good way to do this is to keep digital copies of all your tax documents filed somewhere safe. You may need this number again next year when filing taxes.

In Conclusion,

Don’t go into taxes without knowing about the different types of income, income calculations, and how they relate to your tax return. This will help you be correct in all your tax filing, help you avoid a tax audit, and could even get you better refunds!

Understanding how to calculate your annual income in different ways can also help you budget more precisely. Knowing how to calculate numbers like gross income, adjusted gross income, and net income can help you learn how to calculate your actual take-home pay, for more accurate monthly budget plans.

This content is for informational purposes only and does not constitute financial or legal advice. Loan products, terms, amounts, rates, fees, and funding times may vary by state and applicant qualifications. All loans are subject to approval and verification under applicable law. Check City is a licensed lender in each state where it operates. Loans are intended for short-term financial needs only. Please borrow responsibly.